The Macroeconomic Determinants of Moroccan Corporate Bankruptcy

Youssef Zizi1*

Mohamed Oudgou2

Abdeslam El Moudden3

1,3ENCG Kenitra, Ibn Tofail University, Kenitra, Morocco. |

AbstractThe absence of prior research in Morocco using the macroeconomic explanatory approach to bankruptcy, combined with the new peak in business failure in Morocco in 2021, motivates the need to explore the influence of macroeconomic indicators on the Moroccan bankruptcy rate. Therefore, the objective of this article is to examine the impact of these indicators on the Moroccan bankruptcy rate using multiple regression models over the period 2010-2021. The obtained results show that new firm creation and the interest rate positively and significantly affect the bankruptcy rate, while Euro and Dollar exchange rates have negative and significant effects on the dependent variable. The results suggest guidelines for policymakers and practitioners to refine the economic conditions in order to achieve a low bankruptcy rate in Morocco. |

Licensed: |

|

Keywords: JEL Classification |

|

Received: 30 May 2022 |

Funding: This study received no specific financial support. |

Competing Interests:The authors declare that they have no competing interests. |

1. Introduction

The literature on business failure dates back to the works of Fitzpatrick (1932) and Smith and Winakor (1935) in the 1930s. Several empirical studies have been published on this topic in different study contexts (Shi & Li, 2019). One of the main motivations for these studies is to allow practical decisions to be made based on the obtained results (Ball & Foster, 1982).

Business failure is a complex concept with a multitude of definitions. Bankruptcy refers to the ultimate stage of business failure and constitutes its legal definition. Refait-Alexandre (2004) defined bankruptcy as the opening of legal proceedings following a situation of default. In Morocco, business failures reached a peak of 10,556 in 2021, having increased by 58.62% compared to 2020. The number of bankruptcies recorded in Morocco in 2021 was a new national record (Inforisk, 2022). Bankruptcy results in significant direct and indirect costs to creditors, shareholders, and other stakeholders. In addition, bankruptcies can have adverse macroeconomic effects (Hazak & Mannasoo, 2007). Nevertheless, the majority of studies on business failure in general, and bankruptcy in particular, have been based on the analysis of microeconomic data (Ben Jabeur, Mefteh-Wali, & Carmona, 2021). This is also the case in the Moroccan context, where a limited number of studies on business failure have examined the impact of financial ratios (Azayite & Achchab, 2017; Bahrin, Yusuf, Muhammad, & Ghani, 2022; Obeid 2022; Zizi, Oudgou, & Moudden, 2020) without considering the impact of macroeconomic indicators. Therefore, there is a need to explore the effect of these indicators on bankruptcy in Morocco. Indeed, several studies have shown that the introduction of macroeconomic variables in econometric models leads to a better understanding and increases the models’ predictive power of bankruptcy (Habib, Costa, Huang, Bhuiyan, & Sun, 2020). The objective of the paper is to examine the influence of macroeconomic indicators on the Moroccan bankruptcy rate. Hence, this article aims to answer the following two questions: What are the macroeconomic determinants of bankruptcy in Morocco? How do macroeconomic indicators influence the bankruptcy rate in Morocco? To answer these questions, multiple regression models are used to determine the influence of macroeconomic variables, namely new firm creation, Gross Domestic Product (GDP), Consumer Price Index (CPI), money supply (M3), interest rate, Euro exchange rate, and Dollar exchange rate, on the bankruptcy rate in Morocco in the period 2010-2021. This article’s contributions to the literature are twofold. To the best of our knowledge, this study is the first to explore the impact of macroeconomic variables on the Moroccan bankruptcy rate. Second, the results suggest that interest rate and new firm creation impact positively and significantly the Moroccan bankruptcy rate while Euro and Dollar exchange rates have a significant negative effect. The remainder of this article is organized as follows. Section 2 reviews the previous literature on the macroeconomic approach to business failure. In Section 3, the research methodology is presented, including the data, variable definitions, and model presentation. Sections 4 and 5 deal with the empirical results and their discussion, respectively. Finally, the conclusions of the paper are presented in Section 6.

2. Literature Review

The macroeconomic approach must be considered one of the main explanatory approaches to business failure. Indeed, changes in macroeconomic indicators and economic conditions increase the risk of corporate insolvency – hence, the importance of considering these approaches (Kristanti, Rahayu, & Isynuwardhana, 2019). Nevertheless, the macroeconomic causes of business failure have been neglected in most previous studies (Liu, 2004). In fact, these works have been based solely on the financial explanatory approaches to business failure (Bellovary, Giacomino, & Akers, 2007; Mselmi, Lahiani, & Hamza, 2017; Zizi, Jamali-Alaoui, El Goumi, Oudgou, & El Moudden, 2021) . In the last decade, several studies have focused on the use of macroeconomic variables to explain and predict corporate failure (Ben Jabeur et al., 2021). These studies have shown that macroeconomic factors, namely economic conditions, business creation, inflation, and interest rate, significantly influence business failure (Jiang & Jones, 2018; Khoja, Chipulu, & Jayasekera, 2019; Tinoco & Wilson, 2013) .

The survival of a firm may depend on economic conditions. Difficult economic conditions can increase the risk of bankruptcy due to declining business and profitability indicators (Liou & Smith, 2007). In fact, the clearing effect during periods of economic recession results in firms that are less profitable and less adapted to their environment disappearing at a higher rate than in normal economic contexts (Fougère, Golfier, Horny, & Kremp, 2013). According to Marco (1984), there is a systematic correlation between economic recessions and French business failures. Pearce II and Michael (2006) confirmed the clearing effect of periods of economic recession. According to these authors, in the years after 1990, more than 500,000 American firms went bankrupt in the economic recessions experienced by the United States. Several studies have shown that GDP is a significant and relevant determinant of business failure in different economic contexts (Benito, Delgado Rodriguez, & Martinez Pagés, 2004; Bunn & Redwood, 2003; Hol, 2007) . Hudson (1986) and Ilmakunnas and Topi (1999) demonstrated that GDP growth is negatively related to business failure rates. Similarly, Jardim and Pereira (2013) showed that GDP negatively influences the bankruptcy rate of Portuguese firms.

Superficially, periods of economic growth should favor the creation and development of businesses, leading to fewer legal failures. However, the basic observation is that there is a positive correlation between the growth and suppression rate and the creation and disappearance rate (Dunne, Roberts, & Samuelson, 1989; Stef & Jabeur, 2018). According to Jayet and Torre (1994), the periods and geographic areas with the highest creation rates are also those with the highest exit rates. Several studies have suggested the rate of firm creation as an explanatory variable of firm mortality (Altman, 1983; Malecot, 1988). Using US industrial census data for the period 1963-1982, Dunne et al. (1989) found that the sectors most affected by business failure were those with the highest creation rates. Fleury (1988) confirmed this finding, concluding that the French regions with the highest creation rates were those with the highest rates of disappearance of young firms under three years old. Altman (1983) found a positive correlation between the number of business start-ups and bankruptcies. According to the author, this observation seems obvious since young firms are more likely to disappear due to the liability of newness. Inflation is a widely used macroeconomic indicator in business failure prediction studies. However, the impact of inflation on business mortality remains ambiguous (Jones, Johnstone, & Wilson, 2015). In the short term, inflation can have a positive impact on over-indebted companies since it allows them to repay their debts with depreciated money (Altman, 1983). For Muchtar, Rahmidiani, and Siwi (2016), inflation improves the economy and prevents sluggishness. Nevertheless, poor anticipation of inflation can create liquidity problems for firms and can ultimately lead to bankruptcy (Wadhwani, 1986). Khoja et al. (2019) explained the adverse effects of inflation on the economy by the inability of credit markets to regulate debt levels with inflation. In line with these findings, Tinoco and Wilson (2013) identified that the inflation measure used for banks' default predictions positively impacts the probability of default.

Several authors have demonstrated the significant impact of interest rates on business failure rates in several countries (Grimshaw, 1979; Hall & Young, 1991; Millington, 1994) . In the United States, Artus and Lecointe (1991) showed that interest rate has a positive impact on business failure. According to these authors, a high default rate is the result of monetary policy that induces an increase in the interest rate rather than an increase in the debt ratio. According to Grimshaw (1979), distressed firms depend particularly on the conditions for obtaining bank credit. Indeed, business failures increase when bank conditions are tightened. Hudson (1989) noted that the interest rate positively and significantly affects the exit rate of firms. Wadhwani (1986) found that the number of liquidations is positively correlated with interest rates. Through the error-correction model, Liu (2004) identified that interest rates and creation rates are determinants of firm failure in both the short and long run for UK firms.

3. Methodology

3.1. Data

This study investigated the influence of macroeconomic variables on the Moroccan bankruptcy rate over the period 2010-2021. This period was chosen due to the absence of official statistics on business failure in Morocco before 2010. The data were extracted from different sources, namely, The World Bank, Bank Al-Maghrib, Inforisk, and the OMPIC.

3.2. Definition of Variables

3.2.1. Dependent Variable

Our variable to be explained was the bankruptcy rate. This variable was measured as the annual increase in bankruptcies in Morocco. This data was obtained from the annual statistics provided by Inforisk. In this study, bankruptcy was defined as the opening of legal proceedings by the commercial court against a firm.

3.2.2. Independent Variables

Concerning the explanatory variables, we examined the impact of macroeconomic indicators on the bankruptcy rate. The chosen explanatory variables were New Firm Creation (NFC), Gross Domestic Product (GDP), Consumer Price Index (CPI), Money Supply (MS), Interest Rate (IR), Euro Exchange Rate (Eur ER), and Dollar Exchange Rate (USD ER). The literature review suggested that these variables affected the occurrence of bankruptcy (Bhattacharjee, Higson, Holly, & Kattuman, 2004; Everett & Watson, 1998; Hazak & Mannasoo, 2007; Jiang & Jones, 2018; Kristanti et al., 2019; Stef & Jabeur, 2018) .

NFC referred to the annual birth rate of firms. This rate was calculated from OMPIC statistics. Moreover, we used Gross Domestic Product (GDP) and the interest rate as traditional explanatory variables for business failure. CPI measured the changes in the prices of consumer goods and services in Morocco. Money supply (M3) measured the level of liquidity of economic agents in Morocco. It included assets that could be used immediately as means of payment, short-term loans, and short-term and long-term deposits. The final two explanatory variables were the Euro and Dollar exchange rates. These two currencies represent the main currencies of international operations in Morocco (Bank Al-Maghrib, 2021).

Table 1 gives a detailed description of the explanatory variables used in this study, including their definitions and sources.

3.3. Multiple Regression (OLS)

In the context of a causal analysis, the study’s objective was twofold: first, to determine whether each selected macroeconomic variable impacted the bankruptcy rate in Morocco; second, to estimate the magnitude of the impact of each significant variable. For these two reasons, we used multiple regression.

Multiple regression attempts to model the change in a dependent variable as a linear function of a set of regressors. This modeling is accomplished using a linear equation that quantifies the contribution of each explanatory variable to the dependent variable via regression coefficients. The parameters in the regression model were estimated using the Ordinary Least Squares (OLS) method.

The linear equation is written as follows:

| Variable | Definition | Source |

| New Firm Creation (NFC) | Annual birth rate of firms in Morocco | OMPIC |

| Gross Domestic Product (GDP) | Annual growth of GDP (Current US dollars) | World Bank |

| Consumer Price Index (CPI) | Annual percentage change in CPI | World Bank |

| Money Supply (MS) | Annual evolution of the money supply (M3) | Bank Al-Maghrib |

| Interest Rate (IR) | Lending rate | Bank Al-Maghrib |

| Euro Exchange Rate (Eur ER) | Euro exchange rate to Moroccan Dirham | Bank Al-Maghrib |

| Dollar Exchange Rate (USD ER) | Dollar exchange rate to Moroccan Dirham | Bank Al-Maghrib |

4. Results

4.1. Descriptive statistics

Table 2 presents the descriptive statistics of the study variables. For the dependent variable, the annual increase in bankruptcies, the table shows that the maximum change recorded was 59%. This corresponded to the year 2021, which set a new record for bankruptcies in Morocco (Inforisk, 2022). Similarly, the annual rate of new firm creation showed the greatest change in 2021, with a 23% increase. The annual bankruptcy and new firm creation rates recorded falls of 21% and 11%, respectively, in 2020. The fall in bankruptcies in 2020 is explained by the exceptional measures1 put in place by the State to support businesses in difficulty during the pandemic and the almost continuous closure of the commercial courts between March and September 2020 (Inforisk, 2021). Regarding the Gross Domestic Product (GDP), the largest increase (9.00%) was recorded in 2011, while in 2015 the GDP experienced a decrease of 8%. Moreover, the descriptive statistics show that the means of the Consumer Price Index (CPI) and money supply were 1% and 5%, respectively, while the average interest rate was 6%. Finally, the exchange rates of the Euro and US Dollar to Moroccan Dirham ranged from 10.51 to 11.30 and from 8.09 to 9.80, respectively.

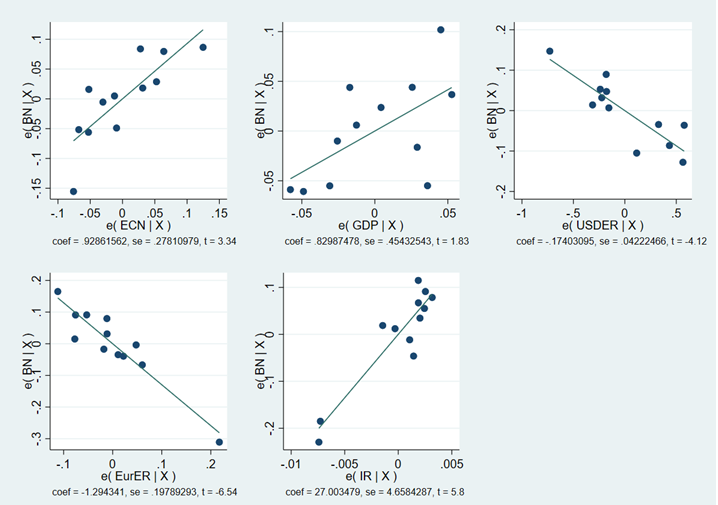

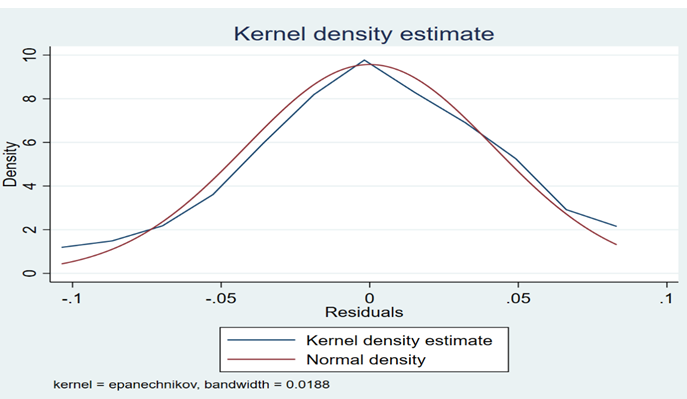

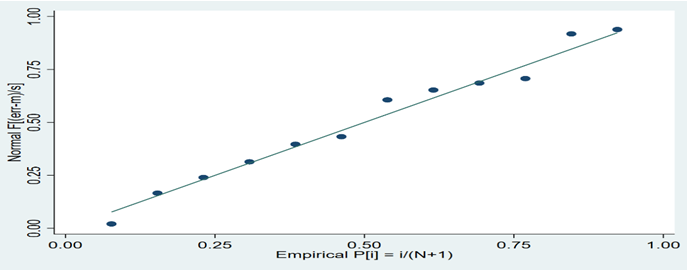

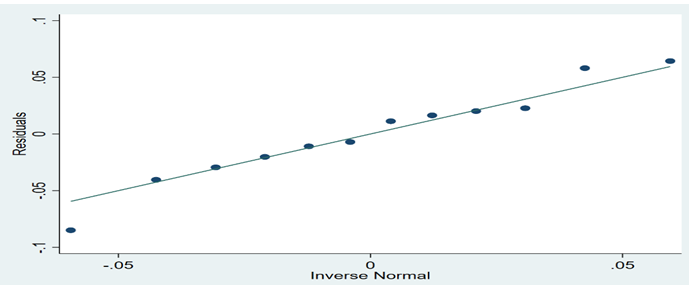

Table 3 shows that there are significant correlations at the 10% threshold, such as those between new firm creation and the bankruptcy rate and between the Euro exchange rate and the interest rate. Therefore, we tested the degree of multicollinearity to ensure that the significant correlations did not affect the results. As shown in Table 4, all VIF values are less than 10 and their tolerances are above 0.1. Thus, there is no multicollinearity problem. Appendices 1, 2, 3, 4, and 5 illustrate the multiple regression assumption tests.

| Variables | N |

Mean |

SD |

Min |

P25 |

Median |

P75 |

Max |

| BN | 12 |

0.14 |

0.18 |

-0.21 |

0.08 |

0.14 |

0.19 |

0.59 |

| NFC | 12 |

0.05 |

0.09 |

-0.11 |

0.02 |

0.04 |

0.07 |

0.23 |

| GDP | 12 |

0.02 |

0.05 |

-0.08 |

-0.01 |

0.02 |

0.07 |

0.09 |

| CPI | 12 |

0.01 |

0.01 |

0.00 |

0.01 |

0.01 |

0.02 |

0.02 |

| MS | 12 |

0.05 |

0.02 |

0.03 |

0.04 |

0.05 |

0.06 |

0.08 |

| IR | 12 |

0.06 |

0.01 |

0.04 |

0.05 |

0.06 |

0.06 |

0.06 |

| Eur ER | 12 |

10.99 |

0.23 |

10.51 |

10.80 |

11.02 |

11.20 |

11.30 |

| USD ER | 12 |

9.03 |

0.63 |

8.09 |

8.41 |

9.09 |

9.65 |

9.80 |

| Variables | BN |

NFC |

GDP |

CPI |

MS |

IR |

Eur ER |

USD ER |

| BN | 1.000 |

|||||||

| NFC | 0.708* |

1.000 |

||||||

| GDP | 0.094 |

0.313 |

1.000 |

|||||

| CPI | 0.299 |

0.459 |

0.097 |

1.000 |

||||

| MS | -0.369 |

-0.410 |

-0.248 |

-0.448 |

1.000 |

|||

| IR | -0.024 |

-0.270 |

0.193 |

0.071 |

-0.296 |

1.000 |

||

| Eur ER | -0.425 |

-0.404 |

0.391 |

-0.061 |

-0.027 |

0.823* |

1.000 |

|

| USD ER | 0.090 |

0.311 |

-0.276 |

0.148 |

-0.078 |

-0.625* |

-0.765* |

1.000 |

Note: * p <0.1. |

| Variables | VIF |

1/VIF |

| Eur ER | 7.41 |

0.13 |

| IR | 3.69 |

0.27 |

| USD ER | 2.42 |

0.41 |

| GDP | 2.02 |

0.49 |

| NFC | 1.94 |

0.51 |

| Mean VIF | 3.50 |

4.2. Regression Results

The estimation results of the multiple regression models are presented in Table 5. Indeed, this table illustrates five models. The first model presents a simple regression model with a single explanatory variable, new firm creation. The second model shows a multiple regression model with economic variables. The third shows a multiple regression with financial variables. The fourth model represents a global model including all the explanatory variables of the study. Finally, the last model shows the estimation results by stepwise selection technique after introducing all the independent variables.

The variable new firm creation remains significant at least at the 5% level in the four models that include it. This variable has a positive impact on the bankruptcy rate. For example, in the second model, a one-unit increase in this variable can increase bankruptcy by 1.66%. The other two economic variables, the Gross Domestic Product (GDP) and the Consumer Price Index (CPI), do not have a significant effect on bankruptcy. The integrated financial variables keep the same sign in all models and remain significant, except for the money supply variable. The latter was eliminated by the stepwise technique. An increase in the interest rate may lead to a considerable increase in bankruptcy among Moroccan firms. Indeed, this variable positively impacts the annual bankruptcy rate and has the largest marginal effect in both global models. For instance, a rise in this variable can raise the bankruptcy rate by 30.46% in the fourth model. There is a negative relationship between the bankruptcy rate and the exchange rate variables. These two variables were retained by the stepwise selection technique and are at least significant at the 5% threshold in the global models 4 and 5.

Models 4 and 5 present the best goodness-of-fit with coefficients of determination R2 of 0.96 and 0.95, respectively.

M1 |

M2 |

M3 |

M4 |

M5(SW) |

|

| NFC | 1.528 (0.481)*** |

1.666 (0.623)** |

0.999 (0.337)** |

0.929 (0.278)** |

|

| GDP | -0.495 (0.892) |

0.972 (0.508) |

0.830 (0.454) |

||

| CPI | -1.497 (9.950) |

0.836 (4.387) |

|||

| MS | -2.612 (3.011) |

1.876 (1.678) |

|||

| IR | 21.926 (11.285)* |

30.464 (5.862)*** |

27.003 (4.658)*** |

||

| Eur ER | -1.257 (0.371)** |

-1.361 (0.222)*** |

-1.294 (0.198)*** |

||

| USD ER | -0.184 (0.099) |

-0.166 (0.046)** |

-0.174 (0.042)*** |

||

| _cons | 0.059 (0.047) |

0.079 (0.112) |

14.532 (4.207)** |

14.722 (2.415)*** |

14.365 (2.213)*** |

| R2 | 0.50 |

0.52 |

0.68 |

0.96 |

0.95 |

| N | 12 |

12 |

12 |

12 |

12 |

Note: * p <0.1; ** p <0.05; *** p <0.01. |

5. Discussion

Unlike several studies that have shown that GDP growth and inflation measures significantly influence the probability of bankruptcy (Hazak & Mannasoo, 2007; Jardim & Pereira, 2013; Jiang & Jones, 2018; Kristanti et al., 2019) , this study has shown that these two variables have a positive but not significant impact on the bankruptcy rate in the global models.

However, the empirical results have shown that four variables do significantly impact the bankruptcy rate of Moroccan firms. Among these four variables, two variables have a positive effect, namely new firm creation and interest rate, while the other two variables, namely Euro and Dollar exchange rates, have a negative effect.

The results reveal that new firm creation positively and significantly impacts the bankruptcy rate in the four models where this explanatory variable was introduced. These results are in line with those of Liu (2009); Jardim and Pereira (2013), and Stef and Jabeur (2018). In a sample of 825 French industrial firms, Stef and Jabeur (2018) found that the emergence of new firms positively and significantly impacted firm liquidation and had a strong predictive power. Similarly, Liu (2009) used the vector error-correction model (VECM) to observe fluctuations in British business bankruptcies and examine the interactions between macroeconomic variables and the number of bankruptcies between 1966 and 2003. The results of this study showed that the increase in business births caused an increase in corporate failures in the medium and long term. These results confirmed the findings of Jayet and Torre (1994) and Fleury (1988), who noted that the periods and geographic areas with the highest corporate birth rates were also those with the highest exit rates.

We further observed that the interest rate had a positive impact and the largest marginal effect on the dependent variable. This result is consistent with the results of Everett and Watson (1998). Through a questionnaire administered to shopping center managers in Australia between 1961 and 1990, the authors found that the business failure rate was positively related to the interest rate. Indeed, an increase in the banks’ credit interest rate creates a difficult situation for Moroccan firms since these firms’ first source of financing is bank credit (High Commission for Planning, 2019). According to Grimshaw (1979), bankruptcies increase when banking conditions are tightened.

Contrary to the results of Bhattacharjee et al. (2004) and Yassine, Ibenrissoul, Snoussi, and Benjouid (2017), in this study, the Euro and Dollar exchange rates negatively and significantly affected the bankruptcy of Moroccan firms. For instance, in the United Kingdom, Bhattacharjee et al. (2004) noted through a competing risks hazard regression model over more than thirty years that firm bankruptcy results from a high exchange rate. In the Moroccan context, Yassine et al. (2017) studied the impact of economic variables on the default rate of Moroccan corporate borrowers based on data from the period 2005-2011. They identified that the Euro and Dollar exchange rates were positively associated with the default rate.

6. Conclusions

Two main motivations led us to conduct this study, namely the new record of business failure set in Morocco in 2021 and the absence of prior research using the macroeconomic explanatory approach to bankruptcy in Morocco. Therefore, the objective of this paper was to examine the influence of macroeconomic indicators on the Moroccan bankruptcy rate.

We used multiple regression models to determine the impact of macroeconomic variables and estimate their effect on the bankruptcy rate in Morocco between 2010 and 2021. The variables introduced to the models were new firm creation, Gross Domestic Product (GDP), Consumer Price Index (CPI), money supply, interest rate, the Euro exchange rate, and the Dollar exchange rate. These variables were selected for their explanatory power identified in the literature review. The data for the explanatory variables were extracted from different databases, namely the World Bank, Bank Al-Maghrib, Inforisk, and OMPIC.

The estimation results showed that four of the seven explanatory variables were significant at the 5% threshold. Both new firm creation and the interest rate had a positive effect on the bankruptcy rate. In addition, the interest rate had the largest marginal effect on the dependent variable. On the other hand, the Euro and Dollar exchange rates negatively affected the Moroccan bankruptcy rate.

The results suggest certain guidelines for policymakers and practitioners to refine the economic conditions in order to achieve a low bankruptcy rate in Morocco.

Nevertheless, the results have some limitations. First, they are limited to a single country, namely Morocco. Second, the selected explanatory variables were all related to the macroeconomic approach. For improvement purposes, in future studies, it would be interesting to include other MENA countries to compare the results obtained in the Moroccan context with those from the wider region. In addition, it would be preferable to include variables representing the managerial approach, such as management and entrepreneurial qualities.

References

Altman, E. I. (1983). Why business fail. Journal of Business Strategy, 3(4), 15-21.Available at: https://doi.org/10.1108/eb038985 .

Artus, P., & Lecointe, F. (1991). Financial crisis and private debt crisis in the United States. French Journal of Economics, 6(1), 37-85.Available at: https://doi.org/10.3406/rfeco.1991.1273 .

Azayite, F. Z., & Achchab, S. (2017). The impact of payment delays on bankruptcy prediction: A comparative analysis of variables selection models and neural networks. Paper presented at the 2017 3rd International Conference of Cloud Computing Technologies and Applications (CloudTech).

Bahrin, N. L., Yusuf, S. N. S., Muhammad, K., & Ghani, E. K. (2022). Determinants of anti-money laundering program effectiveness among banks. International Journal of Management and Sustainability, 11(1), 21–30.Available at: https://doi.org/10.18488/11.v11i1.2939 .

Ball, R., & Foster, G. (1982). Corporate financial reporting: A methodological review of empirical research. Journal of accounting Research, 20, 161-234.Available at: https://doi.org/10.2307/2674681 .

Bank Al-Maghrib. (2021). Annual report of Bank Al-Maghrib for the year 2020. Rabat: Bank Al-Maghrib.

Bellovary, J. L., Giacomino, D. E., & Akers, M. D. (2007). A review of bankruptcy prediction studies: 1930 to present. Journal of Financial Education, 33, 1-42.Available at: http://www.jstor.org/stable/41948574.

Ben Jabeur, S., Mefteh-Wali, S., & Carmona, P. (2021). The impact of institutional and macroeconomic conditions on aggregate business bankruptcy. Structural Change and Economic Dynamics, 59, 108-119.Available at: https://doi.org/10.1016/j.strueco.2021.08.010 .

Benito, A., Delgado Rodriguez, F. J., & Martinez Pagés, J. (2004). A synthetic indicator of financial pressure for Spanish firms. Working Papers / Bank of Spain, No. 0411.

Bhattacharjee, A., Higson, C., Holly, S., & Kattuman, P. (2004). Business failure in UK and US quoted firms: Impact of macroeconomic instability and the role of legal institutions. Cambridge Working Papers in Economics 0420, Faculty of Economics, University of Cambridge.

Bunn, P., & Redwood, V. (2003). Company accounts-based modelling of business failures and the implications for financial stability. Bank of England Working Paper No. 210. London: Bank of England.

Dunne, T., Roberts, M. J., & Samuelson, L. (1989). The growth and failure of US manufacturing plants. The Quarterly Journal of Economics, 104(4), 671-698.

Everett, J., & Watson, J. (1998). Small business failure and external risk factors. Small Business Economics, 11(4), 371-390.

Fitzpatrick, P. J. (1932). A comparison of the ratios of successful industrial enterprises with those of failed companies. Lanzhou: The Certified Public Account.

Fleury, M. (1988). Regions at the forefront of business creation. Economics and Statistics, 215(1), 51–56.

Fougère, D., Golfier, C., Horny, G., & Kremp, É. (2013). What was the impact of the 2008 crisis on business failure? Economics and Statistics, 462(1), 69-97.Available at: https://doi.org/10.3406/estat.2013.10217 .

Grimshaw, A. E. (1979). An empirical examination of the relationship between small business failure rates and macroeconomic conditions. 1979, University of Maryland, D.B.A.

Habib, A., Costa, M. D., Huang, H. J., Bhuiyan, M. B. U., & Sun, L. (2020). Determinants and consequences of financial distress: review of the empirical literature. Accounting & Finance, 60(S1), 1023-1075.Available at: https://doi.org/10.1111/acfi.12400 .

Hall, G., & Young, B. (1991). Factors associated with insolvency amongst small firms. International Small Business Journal, 9(2), 54-63.Available at: https://doi.org/10.1177/026624269100900204 .

Hazak, A., & Mannasoo, K. (2007). Indicators of corporate default: an EU based empirical study (Vol. 10): Eesti Pank Tallinn.

High Commission for Planning. (2019). National business survey, first results 2019. Casablanca: High Commission for Planning.

Hol, S. (2007). The influence of the business cycle on bankruptcy probability. International transactions in operational research, 14(1), 75-90.Available at: https://doi.org/10.1111/j.1475-3995.2006.00576.x.

Hudson, J. (1986). An analysis of company liquidations. Applied Economics, 18(2), 219-235.Available at: https://doi.org/10.1080/00036848600000025 .

Hudson, J. (1989). The birth and death of firms. Quarterly Review of Economics and Business, 29(2), 68–86.

Ilmakunnas, P., & Topi, J. (1999). Microeconomic and macroeconomic influences on entry and exit of firms. Review of Industrial Organization, 15(3), 283-301.

Inforisk. (2021). Inforisk study, insolvencies Morocco 2020. Casablanca: Inforisk.

Inforisk. (2022). Inforisk study, insolvencies Morocco 2021. Casablanca: Inforisk.

Jardim, C. P., & Pereira, E. T. (2013). Corporate bankruptcy of Portuguese firms. Zagreb International Review of Economics & Business, 16(2), 39-56.

Jayet, H., & Torre, A. (1994). Empirical studies-life and death of businesses. Reflections on the dynamics of renewal of economic fabrics. Journal of Industrial Economics, 69(1), 75-91.Available at: https://doi.org/10.3406/rei.1994.1539 .

Jiang, Y., & Jones, S. (2018). Corporate distress prediction in China: A machine learning approach. Accounting & Finance, 58(4), 1063-1109.Available at: https://doi.org/10.1111/acfi.12432 .

Jones, S., Johnstone, D., & Wilson, R. (2015). An empirical evaluation of the performance of binary classifiers in the prediction of credit ratings changes. Journal of Banking & Finance, 56, 72-85.Available at: https://doi.org/10.1016/j.jbankfin.2015.02.006 .

Khoja, L., Chipulu, M., & Jayasekera, R. (2019). Analysis of financial distress cross countries: Using macroeconomic, industrial indicators and accounting data. International Review of Financial Analysis, 66, 101379.Available at: https://doi.org/10.1016/j.irfa.2019.101379 .

Kristanti, F. T., Rahayu, S., & Isynuwardhana, D. (2019). The survival of small and medium business. Polish Journal of Management Studies, 20(2), 311-321.

Liou, D.-K., & Smith, M. (2007). Financial distress and corporate turnaround: A review of the literature and agenda for research. Accounting, Accountability & Performance, 13(1), 74-114.Available at: https://doi.org/10.2139/ssrn.925596 .

Liu, J. (2004). Macroeconomic determinants of corporate failures: evidence from the UK. Applied Economics, 36(9), 939-945.Available at: https://doi.org/10.1080/0003684042000233168 .

Liu, J. (2009). Business failures and macroeconomic factors in the UK. Bulletin of Economic Research, 61(1), 47-72.Available at: https://doi.org/10.1111/j.1467-8586.2008.00294.x .

Malecot, J. F. (1988). Statistical prediction of failure: Questions of methods and practical questions. The Bank Review, 479, 8-12.

Marco, L. (1984). Business failures and the crisis in France (1974-1983). Journal of Political Economy, 94(5), 676-687.Available at: http://www.jstor.org/stable/24698855.

Millington, J. K. (1994). The impact of selected economic variables on new business formation and business failures. Journal of Small Business Finance, 3(2), 177-179.

Mselmi, N., Lahiani, A., & Hamza, T. (2017). Financial distress prediction: The case of French small and medium-sized firms. International Review of Financial Analysis, 50, 67-80.Available at: https://doi.org/10.1016/j.irfa.2017.02.004 .

Muchtar, Rahmidiani, & Siwi. (2016). Banks and other financial institutions. Jakarta: KENCANA.

Obeid , R. (2022). Early warning of bank failure in the Arab region: A logit regression approach. Asian Journal of Economics and Empirical Research, 9(2), 91–99.Available at: https://doi.org/10.20448/ajeer.v9i2.4120 .

Pearce II, J. A., & Michael, S. C. (2006). Strategies to prevent economic recessions from causing business failure. Business Horizons, 49(3), 201-209.Available at: https://doi.org/10.1016/j.bushor.2005.08.008 .

Refait-Alexandre, C. (2004). Prediction of bankruptcy based on the financial analysis of the company: an inventory. Economies Forecasts, 162(1), 129-147.Available at: https://doi.org/10.3406/ecop.2004.6937 .

Shi, Y., & Li, X. (2019). An overview of bankruptcy prediction models for corporate firms: A systematic literature review. Intangible Capital, 15(2), 114-127.Available at: https://doi.org/10.3926/ic.1354.

Smith, R. F., & Winakor, A. H. (1935). Changes in the financial structure of unsuccessful industrial corporations: Urbana, University of Illinois. Bureau of Business Research. Bulletin; No. 51.

Stef, N., & Jabeur, S. B. (2018). The bankruptcy prediction power of new entrants. International Journal of the Economics of Business, 25(3), 421-440.Available at: https://doi.org/10.1080/13571516.2018.1455389 .

Tinoco, M. H., & Wilson, N. (2013). Financial distress and bankruptcy prediction among listed companies using accounting, market and macroeconomic variables. International Review of Financial Analysis, 30, 394-419.Available at: https://doi.org/10.1016/j.irfa.2013.02.013 .

Wadhwani, S. B. (1986). Inflation, bankruptcy, default premia and the stock market. The Economic Journal, 96(381), 120-138.Available at: https://doi.org/10.2307/2233429 .

Yassine, A., Ibenrissoul, A., Snoussi, N., & Benjouid, Z. (2017). Macroeconomic determinants of borrower default: The case of a Moroccan Bank.

Zizi, Y., Oudgou, M., & Moudden, A. E. (2020). Determinants and predictors of smes’ financial failure: A logistic regression approach. Risks, 8(4), 1–21.Available at: https://doi.org/10.3390/risks8040107 .

Zizi, Y., Jamali-Alaoui, A., El Goumi, B., Oudgou, M., & El Moudden, A. (2021). An optimal model of financial distress prediction: A comparative study between neural networks and logistic regression. Risks, 9(11), 200.Available at: https://doi.org/10.2307/2233429.

Appendices

Appendix 1. Partial-regression leverage plot.

Appendix 2. Checking normality of residuals (kernel density estimate).

Appendix 3. Standardized normal probability plot (P-P plot).

Appendix 4. Normal quantile plot (Q-Q plot).

| Variable | Obs. |

W |

V |

z |

Prob>z |

| Err. | 12 |

0.970 |

0.499 |

-1.353 |

0.912 |