Tax Disclosure in Financial Statements: The Case of Indonesia

Arie Pratama1*

Azzallia Putri Pratiwi2

1,2Department of Accounting, Padjadjaran University, Indonesia. |

AbstractTax disclosure has long been of concern to the public. Corporations provide tax disclosure as part of their financial reporting, whether on a voluntary or mandatory basis. However, the level of tax disclosure is still problematic due to the secrecy aspect of taxation. This research was undertaken to better understand the effects of tax avoidance, good corporate governance, industry regulation, and participation in tax amnesty on corporate tax disclosure. This research used data from 422 public Indonesian companies that had published financial statements in the year 2019. The data were analysed using multiple linear regression. The results reveal a negative relationship between tax avoidance and tax disclosure, with lower tax avoidance leading to higher tax disclosure; a positive relationship between both good corporate governance and tax amnesty and tax disclosure, with better corporate governance and tax amnesty leading to higher tax disclosure; and a negative relationship between industrial regulations and tax disclosure, with increased industrial regulations leading to lower corporate tax disclosure. Overall, this research shows that tax disclosure not only reveals tax activities but also reflects the company’s views on tax compliance. |

Licensed: |

|

Keywords: JEL Classification |

|

Received: 20 June 2022 |

Funding: This study received no specific financial support. |

Competing Interests:The authors declare no conflict of interest/competing interest. |

1. Introduction

The disclosure of taxes in financial statements is still deemed unusual, especially for public companies. Although there are differing views on tax disclosure, the practice is crucial as multiple parties require the information. Companies that report their tax obligations require their financial statements to be adjusted to tax provisions to determine the basis of their tax obligations. To prove these obligations, it is not uncommon for further disclosures to be required relating to the company's tax obligations as an entity. Both financial statement audits and tax audits require disclosure and evidence of transactions that form the basis for determining the company's tax obligations. Based on statistics from the Tax Court Secretariat of the Ministry of Finance (2021), tax dispute filings increased between 2014 and 2020 to a total of more than eighty-six thousand cases. The high level of tax disputes arising every year shows the crucial need for companies to prepare this information.

Pomp and Loiselle (1993) stated that the issue of tax disclosure by companies in the United States had been raised by the staff of New York State's Legislative Tax Study Commission in 1987. At that time, legal regulations were adopted to enforce disclosure in the reports provided by companies. Global activists have also asked governments to regulate the disclosure of information relating to how much tax is paid, particularly how much is paid by multinational companies (Christians, 2013). In 2002, a coalition in the United Kingdom organised the Publish What You Pay campaign to obtain tax information disclosure. The disclosure of information on the amount of tax paid is thought to facilitate control over the use of tax collection itself. The high demand for tax disclosure shows the need for extensive information, especially given the low level of existing disclosures and regulatory standards.

The International Accounting Standards Board (IASB), through International Accounting Standard 12 (IAS 12), regulates income tax, including all domestic and foreign taxes. In addition, the standard regulates the withholding of tax payable. Currently, the IASB does not have a stand-alone regulation for tax disclosure in the International Financial Reporting Standards (IFRS). Indonesia uses the IFRS as a reference in its standards and currently uses the Statement of Financial Accounting Standards (SFAS) 46 Income Tax, which regulates tax disclosure within the scope of the income tax information presented in financial statements.

Despite the importance of corporate transparency, research on financial reporting and disclosure costs and benefits is still limited (Leuz & Wysocki, 2016). Tax transparency provides information that the public can use to assess the company's activities. For example, the copper mining industry in Zambia received strong criticism after information on its tax audit was leaked. This industry pays only 0.6% of its profits to the government (Christians, 2013). More research is needed to emphasise the importance of financial reporting and the benefits of providing adequate disclosure through financial statements. Several previous studies have shown that companies voluntarily make many disclosures. Fadila (2018) stated that the increase in voluntary disclosure is in line with the size of the company, and that there are three reasons for large-scale companies to disclose information: (1) the disclosure has a relatively low cost, (2) the disclosure of information facilitates market access and financing, and (3) the disclosure does not jeopardise the company's position. In addition to company scale, other factors affect the voluntary disclosure of information. Probohudono, Sudaryono, Sumarta, and Ardilas (2015) showed that the proportion of independent directors, managerial ownership, institutional ownership, foreign ownership, and obligatory tax disclosures are related to voluntary financial disclosure. These factors ensure that the company itself is interested in making disclosures and will do so voluntarily. The study also revealed that voluntary financial disclosure by companies includes tax disclosures. Each year, tax disclosure increases along with the percentage of voluntary financial disclosure; from 2009 to 2012 this increase was 59.90%. Christians (2013) stated that multinational companies need to support tax transparency by engaging in voluntary compliance. The World Bank Report published in 2011 notes that fifty of the world's largest oil, gas and mining companies participate in the Extractive Industries Transparency Initiative (EITI) programme, which supports the tax transparency movement through public publication.

Mgammal and Ku (2015) argued that few previous studies had measured tax disclosure because the various measurements depend on the availability and usefulness of data. According to Bapepam-LK rule No.X.K.6, tax disclosures that support the quality of public companies’ financial reports must include at least the following: the relationship between income tax and commercial profits, fiscal reconciliation and current tax accounting, and a statement on how taxes result from the fiscal reconciliation, which is the basis for corporate tax reporting. The lack of research and standards makes it difficult to measure whether or not a company’s disclosures are adequate. Until now, the burden of comprehensive disclosure has been on the company. Mgammal and Ku (2015) stated that the comprehensive disclosure of corporate taxes is a concern since it can benefit competitor companies that are not required to make the same disclosure. Disclosure is also thought to bring about other indirect costs to participants and other parties in the capital market (Leuz & Wysocki, 2016). Research has shown a high tendency for investors to only pay attention to companies’ value without considering companies’ tax avoidance behaviours. This is also an obstacle to highlighting the importance of including tax disclosure in financial statements because there is a concern that investors want high company value through high company profits and ignore how companies carry out their tax obligations.

A tax amnesty programme encourages taxpayers to make disclosures and increases information transparency. To support this programme in the long term, the Indonesian Institute of Accountants issued PSAK 70 on Accounting for Tax Amnesty Assets. Siahaan and Martani (2020) found that of the 194 companies that participated in tax amnesty, 111 did not disclose the ransom payment, and 29 did not present the assets and liabilities of the tax amnesty in their financial statements. If the Indonesian Directorate General of Taxes (DGT) wants to increase transparency and accountability, PSAK 70 is thus insufficient. Companies tend not to make disclosures because the person who assesses the immateriality of the company’s tax amnesty assets and liabilities under PSAK 70 does not need to be disclosed. Pratama (2017) stated that the level of fulfilment of formal taxpayer obligations is still relatively low from year to year, with corporate taxpayer compliance at only 49.74% in 2015. Pratama (2017) argued that tax amnesty is a state effort to implement good governance through public policies based on the principles of accountability, transparency and participation. Good corporate governance is also related to company value. Ilmi, Kustono, and Sayekti (2017) stated that company value could be increased through management's ability to effectively and efficiently manage company resources. According to Cheung, Jiang, and Tan (2010), companies' disclosures are one of the most fundamental elements of good corporate governance. The quality of corporate governance is considered important to obtain reliable information (Harisa, Mohamad, & Meutia, 2019).

Currently, the accounting standards for regulating adequate tax disclosure are inadequate. Prior research relating to tax disclosure in financial statements is also minimal. This study contributes to an explanation of the variables that influence the tax disclosure level and aims to explain the current gap in the tax disclosure level in financial statements. The rest of the paper is organised as follows: Section 2 presents a brief literature review and the research hypotheses, Section 3 describes the research method, Section 4 provides the research results, implications and a discussion, and Section 5 concludes the article.

2. Literature Review and Hypotheses Development

Financial reporting and disclosure can be valuable managerial tools to communicate corporate governance and performance to investors (Healy & Palepu, 2001). According to Spasić and Denčić-Mihajlov (2014), financial reporting is a communication process involving the exchange of financial and non-financial information between organisations and their surroundings. Information availability is critical in closing the information gap between internal and external stakeholders (Cheung et al., 2010). As a standard that regulates financial reporting, IFRS plays a significant role in regulating the information that must be provided to describe the actual accounting and economic situation (Pratama, 2018). Disclosure can increase and accelerate the spread of information to the market and improve the quality of the information provided (Abdullah & Al-Jafari, 2011). Experts have long suspected that humans behave differently when their actions are monitored or disclosed to others (Lunawat, Shields, & Waymire, 2021).

Lunawat et al. (2021) stated that the assumption exists that someone will maximise their utility regardless of other parties. For this reason, the information provided needs to be supported by adequate evidence through financial disclosure. According to Pomp and Loiselle (1993), disclosure increases the openness of and accountability for the information disclosed. Tax information is a type of information that needs to be disclosed in financial statements. Disclosure of tax information is carried out by providing a point of view based on concepts, theories, limitations, benefits and current and past measurements (Mgammal & Ku, 2015). Furthermore, Mgammal and Ku (2015) asserted that tax reform movements are widely known to have the main goal of ensuring that the public receives this information.

Various factors affect a company’s level of disclosure of tax information, although the public and the government pay more attention to business activities that threaten tax practices (Handoyo, Wicaksono, & Darmesti, 2022; Hoopes, Robinson, & Slemrod, 2018; Tambun & Haryati, 2022) . Desai and Dharmapala (2006) argued that the significant influence of managers causes a relationship between corporate tax avoidance and incentives. (Hasegawa, Hoopes, Ishida, & Slemrod, 2013) argued that non-universal disclosures have consequences, meaning that taxpayers will try to avoid the disclosure obligation by reducing the company's taxable profit. Kubick, Lynch, Mayberry, and Omer (2016) found that companies have lower levels of involvement in tax avoidance as disclosure quality increases. On the other hand, the implementation of corporate governance related to the company's ownership structure shows that institutional ownership drastically increases disclosures (Mais & Patmaningsih, 2017). Pillai and Al-Malkawi (2018) argued that despite different corporate governance systems around the world, capital owners expect a mechanism that ensures disclosure and transparency from companies. Concerning tax amnesty, Siahaan and Martani (2020) found that tax amnesty participants tend to make diverse and limited presentations and disclosures regarding tax amnesty in the notes to financial statements. Such disclosures tend to take the form of qualitative and narrative information, making objective measurements difficult (Leuz & Wysocki, 2016).

Oats and Tuck (2019) regarded transparency as a costly regulatory strategy, not only for information providers but also for those who need to process or evaluate the information. There are costs associated with complying with information-provision regulations as well as costs of monitoring compliance with regulatory requirements on tax transparency. In their research, Hasegawa et al. (2013) found that Japanese companies tend to try to minimise taxable income to avoid the costs associated with tax disclosure. For this reason, increasing taxpayer willingness to make tax disclosures is necessary, and it is important to ensure that there are benefits that are commensurate with the costs incurred when making disclosures. According to Leuz and Wysocki (2016), regulations governing disclosure obligations are not needed if voluntary disclosure offers benefits greater than the disclosure costs.

Christians (2013) stated that the immediate goal of transparency is public knowledge of the revenues received by the government and accountability for the use of these revenues. In contrast, some companies expect financial statements to function as a way to attract investors. A study of transparency in listed companies in the Republic of China showed a significant positive relationship between transparency and the market value of companies (Cheung et al., 2010). According to a bill filed in the United States in April 2003, the benefits of an order to disclose income taxes for US public companies are to facilitate the analysis of financial statements as permission to examine the truth about tax liabilities; to review corporate taxation strategies as a way to avoid tax avoidance activities; and to make an effort to restrain tax avoidance (Hasegawa et al., 2013).

2.1. Tax Avoidance and Tax Disclosure

Corporate tax avoidance has attracted public attention since the 2008 global economic crisis (Oats & Tuck, 2019). Countries are trying to support the transparency demanded by activists and non-profit organisations. For example, since 2016, the United Kingdom has carried out tax reforms that require specific categories of companies to make separate disclosures related to corporate taxation strategies, and it has seen a significant increase in voluntary disclosures in annual reports. Nevertheless, no broad effect has been found on tax avoidance (Bilicka, Eberhard, Seregni, & Stage, 2021). Bilicka et al. (2021) stated that companies with low reporting quality have higher rates of tax evasion. In the United States, a Securities and Exchange Commission (SEC) comment letter was issued to companies, requiring additional disclosure. Kubick et al. (2016) stated that this additional disclosure request could reduce the level of tax avoidance. Companies with a high level of tax avoidance tend to avoid tax disclosure; thus, when there is a demand for tax disclosure, a company’s level of tax avoidance tends to decrease. Hence, the first hypothesis is:

H1: The tax avoidance variable has an effect on the level of corporate tax disclosure.

2.2. Good Corporate Governance and Tax Disclosure

Good corporate governance attracts more attention when there is an increase in financial scandals in the business environment (Mais & Patmaningsih, 2017). Corporate governance, as an internal and external system that ensures corporate accountability, guarantees and improves disclosure quality (Abdelfattah & Aboud, 2020; Pratama, 2018).

Altamuro and Beatty (2010) also argued that internal control has become the recommended mechanism for creating quality financial reports. Good corporate governance is considered a necessary internal control mechanism to balance the external monitoring carried out by tax officials (Kovermann & Velte, 2019). This relates to the disclosure regulations imposed on the company by the regulator.

Desai and Dharmapala (2006), quoted in Armstrong, Blouin, Jagolinzer, and Larcker (2015), stated that companies with good governance tend to have internal controls to avoid deviant management activities. Such deviation is related to management activities that further individual interests by ignoring regulations and company obligations. Christians (2013) argued that the tax transparency movement will demonstrate global governance in tax law. Hence, the second hypothesis is:

H2: The variables of good corporate governance have an effect on the level of corporate tax disclosure.

2.3. Industry Regulation and Tax Disclosure

Industrial regulations are a type of control that is imposed by external parties. In this case, industrial regulations can be imposed by the government, specific industry organisations or associations, or other parties to create a good business climate. Different regulations work to provide the best potential environment for the industry.

Differences in regulations or legal requirements in financial disclosures, external audits and corporate taxes can also influence management decisions in the affected companies (Jung & Chung, 2014). Regulation is also capable of mitigating low-quality disclosures related to information overload or lack of information (Leuz & Wysocki, 2016).

The more comprehensive the regulations governing disclosures in financial statements, the more the quality and quantity of corporate tax disclosure will increase. Hence, the third hypothesis is:

H3: The industrial regulation variables have an effect on the level of corporate tax disclosure.

2.4. Tax Amnesty Participation and Tax Disclosure

Pratama (2017) stated that tax amnesty is a programme that guarantees legal certainty by creating more transparent relations between the government, the private sector and the community. Tax amnesty as a programme also impacts the value and volume of company shares (Wibowo & Darmanto, 2017). If the programme is considered attractive by investors, the company's participation rate will be high, and the opportunity for greater transparency will increase. This programme allows for increased tax disclosure in the short and long term.

When participating in this programme, companies adjust their taxpayer financial statements, the provisions of which are regulated in SFAS 70, which covers Accounting for Tax Amnesty Assets and Liabilities. Later, the assets disclosed in the tax amnesty programme will be prospectively reported and disclosed in the financial statements (Indonesian Institute of Accountant, 2016). The tax amnesty programme, which encourages taxpayer transparency, is expected to correlate with the level of corporate tax disclosure. Hence, the fourth hypothesis is:

H4: The participation variables in the tax amnesty programme have an effect on the level of corporate tax disclosure.

3. Methodology

The data used were taken from the financial statements of companies listed on the Indonesia Stock Exchange (ISE) in the 2019 financial year; these were obtained through the www.idx.co.id portal, along with data from company portals.

This study population comprised the companies listed on the ISE in 2019. The number of these companies was 671, meaning that the study’s target sample was 442 companies. The target was based on companies registered in 2019 that did not experience losses in that period and had an effective tax rate (ETR) <1. The reason for choosing 2019 was that ISAK 34, which related to the disclosure of uncertainty about income tax treatment, was enacted in 2018 but only became effective in 2019. The years 2020 and beyond were not chosen due to the COVID-19 pandemic, which meant that several tax variables, both dependent and independent, could have been outliers.

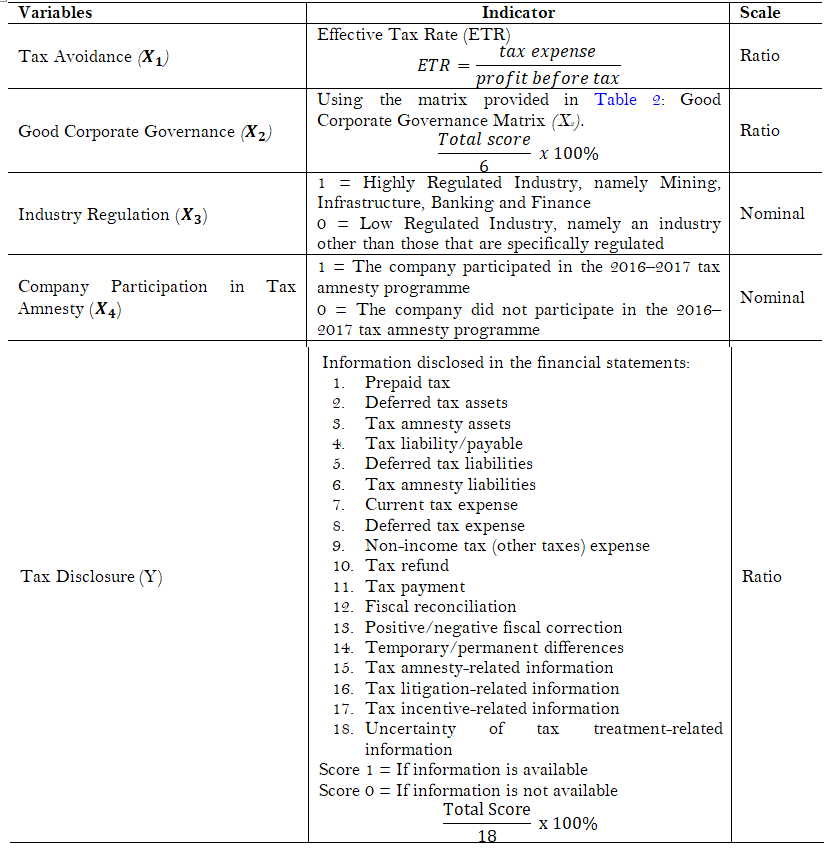

The operational variables of this study are presented in Table 1:

No. |

Criteria | Score 2 | Score 1 | Score 0 |

1 |

Composition of independent commissioners | ≥30% of the entire board of commissioners | <30% of the entire board of commissioners | Does not have an independent commissioner |

2 |

Number of commissioners | ≥ 5 people | < 5 people | Does not have a commissioner |

3 |

Number of people on the audit committee | ≥ 3 people | < 3 people | Does not have an audit committee |

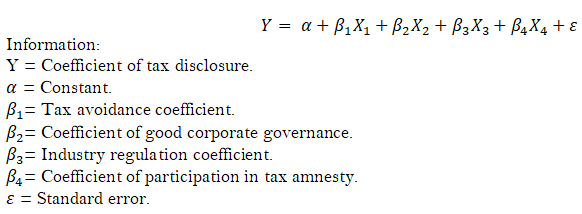

The research data were analysed using the multiple regression method and the following regression equation:

4. Results and Discussions

4.1. Results

The descriptive statistics of the variables are presented in Table 3:

The Effective Tax Rate for companies listed on the Indonesia Stock Exchange in 2019, which is used as a standard measure of tax avoidance activities, shows an average of 0.263 with a standard deviation of 0.184. The number 0.263 indicates that the current effective tax rate is 26%, which means it has exceeded the applicable tax rate of 25%.

| Good Corporate Governance | Maximum |

Minimum |

Average |

Standard Deviation |

| Composition of Independent Commissioners | 75% |

0% |

41% |

0.137 |

| Number of Commissioners | 10 |

2 |

4 |

1.670 |

| Number of Audit Committee | 7 |

0 |

3 |

0.625 |

Table 4 presents the descriptive statistics for the good corporate governance variable. Good corporate governance by companies listed on the IDX in 2019 was measured through several assessment components, including the composition of independent commissioners, the number of commissioners and the number of people on the audit committees. The results show that the average value of good corporate governance is 0.864, which means that the average company has met the good corporate governance standards of more than 80% with a standard deviation of 0.124. When viewing each measurement component of good corporate governance, the ratio of independent commissioners is on average 41% of the entire board of commissioners, whereas the current standard for companies is to have at least 30% independent commissioners on the board. The results also show that the company's average number of commissioners was four, with a maximum of 10 commissioners and a minimum of two. The standard deviation of the number of commissioners is 1.67. Concerning the number of audit committee members, on average, companies had three audit committee members, with a maximum of seven members and a minimum of 0, and a standard deviation of 0.625.

| Industry Regulation | Total |

Percentage |

| Highly Regulated Company | 118 |

27% |

| Non-Highly Regulated Company | 324 |

73% |

Table 5 presents the number of companies in each category of industry regulation. Concerning the industrial regulation variables, the average and standard deviation components cannot be calculated since these variables were measured using the dummy values of one and zero. The value of one (1) was given to companies in the mining, infrastructure, and banking and finance industries, with a total of 118 companies or 27% in this strictly regulated category. Companies in other industries were given a value of zero, with a total of 324 companies or 73% in this category.

| Tax Amnesty | Total |

Percentage |

| Participating Companies | 155 |

35% |

| Non-Participating Companies | 287 |

65% |

Table 6 presents the breakdown of the tax amnesty variable. Means and standard deviations could not be calculated for this variable, as companies were given dummy values of one or zero. The value of one (1) was given to companies that participated in the 2016‒2017 tax amnesty programme, which amounted to 155 companies or 35%. The 287 companies (65%) that did not participate in the programme were given a score of zero. Participation in the programme influenced the disclosures made by the company in that the company showed its openness by voluntarily reporting assets that had not previously been recognised in financial statements. In this way, the company was not constrained from disclosing tax information in its financial statements.

| Tax Disclosure | % |

| Prepaid Tax | 82.81% |

| Deferred Tax Asset | 87.10% |

| Tax Amnesty Asset | 28.51% |

| Tax Liability | 99.55% |

| Deferred Tax Liabilities | 66.52% |

| Tax Amnesty Liabilities | 0.45% |

| Current Tax Expense | 95.70% |

| Deferred Tax Expense | 93.44% |

| Non-income Tax Expense | 93.67% |

| Tax Refund | 47.06% |

| Tax Payment | 97.29% |

| Fiscal Reconciliation | 97.96% |

| Fiscal Correction | 10.41% |

| Differences | 86.43% |

| Tax Amnesty Information | 29.19% |

| Tax Litigation Information | 57.92% |

| Tax Incentive Information | 37.78% |

| Uncertainty Tax Treatment | 30.09% |

Table 7 presents a breakdown of the tax disclosure scores. The average value of tax disclosures by companies listed on the IDX in 2019 was 0.634 or 63.4% of the components used to measure disclosure, with a standard deviation of 0.122. The highest value obtained by a company was 0.944 or 94.4%, with only one component not disclosed by the company, meaning that the company did not encounter obstacles in disclosing its tax obligations. The lowest value obtained by a company was 0.111 or 11.1%, where only two tax components were disclosed in the company's financial statements. When viewing the data per component, tax liability or tax debt was disclosed by 99.55% of companies. This shows that it is considered necessary for a company to disclose tax debt, and companies face no significant obstacles to disclosing this information. Information that still has a low disclosure rate is tax amnesty liabilities at 0.45%. This means that only a few of the companies that participate in the tax amnesty programme disclose their liabilities and report them in their financial statements.

The results of the study’s multiple linear regression analysis are presented in Table 8. It can be seen that the R2 value generated in this research is 17.6% and that all the results of the F test and t-test are significant at 5%. Thus, the model can be said to be feasible to analyse, and all proposed hypotheses can be accepted.

| Variables | Coefficient |

t-Statistic |

Prob. |

| Constant | 0.419243 |

9.450292 |

0.0000* |

| Tax Avoidance | 0.148432 |

4.603965 |

0.0000* |

| GCG | 0.182964 |

3.963776 |

0.0001* |

| Industrial regulation | -0.034665 |

-3.040988 |

0.0025* |

| Tax Amnesty | 0.077551 |

6.858874 |

0.0000* |

| Adjusted R-Squared | 0.175987 |

||

| Wald F-statistic# | 23.23471 |

||

| Prob (F-Statistic)# | 0.000000* |

||

Notes: |

5. Discussion

The study results indicate that there is a negative relationship between a company’s tax avoidance and its tax disclosure. The first hypothesis in the study is accepted, which means that a decrease in the level of tax avoidance leads to an increase in corporate tax disclosure in financial statements. The role of ETR has been established in research as a measure of the level of corporate tax avoidance. This is in line with the opinion of Oats and Tuck (2019), who stated that tax avoidance means choosing a way to reduce tax obligations. Kovermann and Velte (2019) also found that a low ETR reflects a low tax burden as a result of tax avoidance activities. This is also in line with Mgammal (2019), who found that tax avoidance as part of a company's tax planning to increase after-tax profit can reduce the company's tax disclosures. These activities can mitigate the emergence of the company’s disclosure obligations. Kubick et al. (2016) found that companies with higher levels of tax avoidance may receive SEC comment letters in which the company is asked to improve the quality of the disclosures it reports in its financial statements. On the other hand, Pomp and Loiselle (1993) stated that for opponents of disclosure, the benefits of the public knowing tax information are irrelevant due to the difficulty of understanding information related to corporate tax obligations, which only experts in the field can understand.

The research shows a positive relationship between good corporate governance and tax disclosures made by companies. Increasing the proportion of independent commissioners, the number of commissioners and the number of people on the audit committee can increase a company's tax disclosures. It is possible that a company’s management, as an agent that prepares information, may have a conflict of interest with the users of the information (Healy & Palepu, 2001). Thus, the role of commissioners, especially independent commissioners, is considered to be supervisory in relation to management performance. In their study, Armstrong et al. (2015) stated that the board's independence is closely related to tax decisions made by the company, which can be illustrated through the disclosure of tax information in financial statements. In addition, there is the role of the audit committee, whose task is to assess financial reporting and assist the board of commissioners in carrying out risk management within the company (Mais & Patmaningsih, 2017). The role of both is to ensure that governance in the company is running as it should and is a benchmark of how open management can be in managing the resources of the capital buyer. When a company is well-governed, the company is no longer constrained in increasing transparency, that is, transparency in tax information. This is in line with the role of good corporate governance as an internal control activity capable of increasing the quality of reporting that is voluntarily carried out by the company (Altamuro & Beatty, 2010).

The results show a negative relationship between industrial regulation and tax disclosure by companies. The research used the type of industry to assess whether industries with a high level of regulation increase corporate tax disclosure. The study showed a unique result, in which companies in industries with a high level of regulation disclosed less tax information than companies in industries that did not have high regulation. This could be because the industry regulations are not related to the disclosure of tax information. The company then focuses on fulfilling its obligations concerning specific regulations that do not include tax information. Leuz and Wysocki (2016) stated that regulation is no longer needed when the perceived benefits to the company of making disclosures exceed the costs required to complete the disclosures. It costs a lot of money to comply with strict industrial regulations, so there is a possibility that the disclosure of tax information will not provide more significant benefits than the costs incurred by the industry to make the disclosures. The research of Duarte, Kong, Siegel, and Young (2014) found different results if management tends to avoid disclosure obligations when the authorised regulatory institutions are weak in tackling violations. Thus, strict industrial regulations should increase the disclosure of information by management, especially that related to taxes. In addition, Spasić and Denčić-Mihajlov (2014) found that improving the quality of disclosure as a form of transparency is still very diverse and highly dependent on regulations and governing laws.

Finally, the results of the study indicate that there is a positive relationship between tax amnesty and tax disclosure by companies. The research included determining whether the company participated in the tax amnesty programme or not. Participation in the tax amnesty programme is considered part of the company's transparency in fully disclosing its assets. This results in the study’s fourth hypothesis being accepted when companies that participate in the programme no longer have problems disclosing all their tax information. Pratama (2017) also stated that public participation in the tax amnesty programme shows a willingness to create transparency, a form of which is the disclosure of tax information. Participation in the tax amnesty programme is not without risk since it indicates that there has been non-compliance in the past. Some companies prefer not to explicitly disclose information on the grounds of materiality (Pratama, 2017; Siahaan & Martani, 2020).

6. Conclusion

This research allows several conclusions to be drawn. First, the lower the corporate tax avoidance, the higher the tax disclosure in financial statements. Second, a company's good corporate governance activities can increase the disclosure of tax information. Third, well-regulated industries have lower tax disclosure levels than companies that are less highly regulated. Fourth, companies that participate in the tax amnesty programme are more transparent in carrying out their tax obligations; thus, these companies do not encounter obstacles in disclosing tax information.

These conclusions suggest recommendations for several parties. For the government, the suggestion put forward by the authors is to reassess the current tax disclosure regulations to maximise the supply of tax information to users. Tax information can assist the government's supervision of taxpayers in fulfilling their tax obligations and help the public supervise the government in managing these funds, the output generated from the obligations fulfilled by taxpayers. For the Financial Accounting Standards Board (FASB), the recommendation is to re-evaluate the need for standards governing the disclosure of tax information in financial statements. These standards may include rules for determining tax information in financial statements, tax information through additional disclosure and other standards that make it easier for users of financial statements to access corporate tax information.

References

Abdelfattah, T., & Aboud, A. (2020). Tax avoidance, corporate governance, and corporate social responsibility: The case of the Egyptian capital market. Journal of International Accounting, Auditing and Taxation, 38, 100304.Available at: https://doi.org/10.1016/j.intaccaudtax.2020.100304.

Abdullah, K. A., & Al-Jafari, M. K. (2011). The effect of Sarbanes‒Oxley Act (SOX) on corporate value and performance. European Journal of Economics, Finance and Administrative Sciences, 33(1), 42-55.

Altamuro, J., & Beatty, A. (2010). How does internal control regulation affect financial reporting? Journal of accounting and Economics, 49(1-2), 58-74.Available at: https://doi.org/10.1016/j.jacceco.2009.07.002.

Armstrong, C. S., Blouin, J. L., Jagolinzer, A. D., & Larcker, D. F. (2015). Corporate governance, incentives, and tax avoidance. Journal of Accounting and Economics, 60(1), 1-17.

Bilicka, K., Eberhard, E. C., Seregni, C., & Stage, B. M. (2021). Qualitative information disclosure: Is mandating additional tax information disclosure always useful? ZEW Discussion Papers No. 21-047, ZEW ‒ Leibniz Centre for European Economic Research.

Cheung, Y.-L., Jiang, P., & Tan, W. (2010). A transparency disclosure index measuring disclosures: Chinese listed companies. Journal of Accounting and Public Policy, 29(3), 259-280.Available at: https://doi.org/10.1016/j.jaccpubpol.2010.02.001.

Christians, A. (2013). Tax activists and the global movement for development through transparency. In Miranda Stewart and Yariv Brauner (Eds.), Tax, Law and Development (Vol. 12, pp. 288-315). Chelteham, UK: Edward El-Gar.

Desai, M. A., & Dharmapala, D. (2006). Corporate tax avoidance and high-powered incentives. Journal of Financial Economics, 79(1), 145-179.Available at: https://doi.org/10.1016/j.jfineco.2005.02.002.

Duarte, J., Kong, K., Siegel, S., & Young, L. (2014). The impact of the Sarbanes–Oxley Act on shareholders and managers of foreign firms. Review of Finance, 18(1), 417-455.Available at: https://doi.org/10.1093/rof/rft008.

Fadila, C. (2018). The determinants of voluntary disclosure in Indonesia State-Owned enterprises annual reports. Journal of Development Planning: The Indonesian Journal of Development Planning, 2(3), 274-290.Available at: https://doi.org/10.36574/jpp.v2i3.51.

Handoyo, S., Wicaksono, A. P., & Darmesti, A. (2022). Does corporate governance support tax avoidance practice in Indonesia? International Journal of Innovative Research and Scientific Studies, 5(3), 184–201.Available at: https://doi.org/10.53894/ijirss.v5i3.505.

Harisa, E., Mohamad, A., & Meutia, I. (2019). Effect of quality of good corporate governance disclosure, leverage and firm size on profitability of islamic commercial banks. International Journal of Economics and Financial Issues, 9(4), 189.Available at: https://doi.org/10.32479/ijefi.8157.

Hasegawa, M., Hoopes, J. L., Ishida, R., & Slemrod, J. (2013). The effect of public disclosure on reported taxable income: Evidence from individuals and corporations in Japan. National Tax Journal, 66(3), 571-607.Available at: https://doi.org/10.17310/ntj.2013.3.03.

Healy, P. M., & Palepu, K. G. (2001). Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. Journal of Accounting and Economics, 31(1-3), 405-440.Available at: https://doi.org/10.1016/s0165-4101(01)00018-0.

Hoopes, J. L., Robinson, L., & Slemrod, J. (2018). Public tax-return disclosure. Journal of Accounting and Economics, 66(1), 142-162.Available at: https://doi.org/10.1016/j.jacceco.2018.04.001.

Ilmi, M., Kustono, A. S., & Sayekti, Y. (2017). Effect of good corporate governance, corporate social re-sponsibility disclosure and managerial ownership to the corporate value with financial performance as intervening variables: Case on Indonesia stock exchange. International Journal of Social Science and Business, 1(2), 75-88.

Indonesian Institute of Accountant. (2016). Statements of financial accounting standards No. 70: Ac-counting for tax amnesty asset. Jakarta: Salemba Empat.

Jung, W.-O., & Chung, H. (2014). Organizational form changes: Perspectives of financial disclosure and international tax planning. Journal of the Korean Accounting Association, 23(1), 990-1027.

Kovermann, J., & Velte, P. (2019). The impact of corporate governance on corporate tax avoidance—A literature review. Journal of International Accounting, Auditing and Taxation, 36, 100270.Available at: https://doi.org/10.1016/j.intaccaudtax.2019.100270.

Kubick, T. R., Lynch, D. P., Mayberry, M. A., & Omer, T. C. (2016). The effects of increased financial statement disclosure quality on tax avoidance: An examination of SEC comment letters. The Accounting Review, 91(6), 1751–1780.Available at: https://doi.org/10.2308/accr-51433.

Leuz, C., & Wysocki, P. D. (2016). The economics of disclosure and financial reporting regulation: Evidence and suggestions for future research. Journal of Accounting Research, 54(1), 525-622.Available at: https://doi.org/10.1111/1475-679x.12115.

Lunawat, R., Shields, T. W., & Waymire, G. (2021). Financial reporting and moral sentiments. Journal of Accounting and Economics, 72(1), 101421.Available at: https://doi.org/10.1016/j.jacceco.2021.101421.

Mais, R. G., & Patmaningsih, D. (2017). Effect of good corporate governance on tax avoidance of the company in listed of the Indonesia stock exchange (BEI). STEI Journal of Economics, 26(02), 230-243.

Mgammal, M. H. (2019). Corporate tax planning and corporate tax disclosure. Meditari Accountancy Research, 28(2), 327-364.Available at: https://doi.org/10.1108/medar-11-2018-0390.

Mgammal, M. H., & Ku, I. K. N. I. (2015). Corporate tax disclosure: A review of concepts, theories, constraints, and benefits. Asian Social Science, 11(28), 1-14.Available at: https://doi.org/10.5539/ass.v11n28p1.

Ministry of Finance. (2021). Statistics of tax dispute in tax court. Retrieved from http://www.setpp.kemenkeu.go.id/statistik. [Accessed 10 February 2022].

Oats, L., & Tuck, P. (2019). Corporate tax avoidance: Is tax transparency the solution? Accounting and Business Research, 49(5), 565-583.Available at: https://doi.org/10.1080/00014788.2019.1611726.

Pillai, R., & Al-Malkawi, H. A. N. (2018). On the relationship between corporate governance and firm per-formance: Evidence from GCC countries. Research in International Business and Finance, 44(1), 394-410.Available at: https://doi.org/10.1016/j.ribaf.2017.07.110.

Pomp, R. D., & Loiselle, A. P. (1993). Corporate tax policy and the right to know: Improving state tax pol-icymaking by enhancing legislative and public access. New York: The Fiscal Policy Institute.

Pratama, A. (2017). Machiavellianism, perception on tax administration, religiosity and love of money towards tax compliance: Exploratory survey on individual taxpayers in Bandung City, Indonesia. International Journal of Economics and Business Research, 14(3-4), 356-370.Available at: https://doi.org/10.1504/ijebr.2017.087521.

Pratama, A. (2018). Does corporate governance affect related-party transactions? A study on Indonesian companies listed on the Indonesian stock exchange in 2011-2015. International Journal of Economic Policy in Emerging Economies, 11(5), 470-478.Available at: https://doi.org/10.1504/ijepee.2018.094807.

Probohudono, A. N., Sudaryono, E. A., Sumarta, N. H., & Ardilas, Y. (2015). Ownership, corporate governance and mandatory tax disclosure influencing voluntary financial disclosure in Indonesia. Corporate Ownership & Control, 13(1), 74-83.Available at: https://doi.org/10.22495/cocv13i1p8.

Siahaan, T. D., & Martani, D. (2020). Analysis of tax amnesty implementation in the financial statements of publicly listed companies in Indonesia. Paper presented at the KnE Social Sciences: The 3rd International Research Con-ference on Economics and Business.

Spasić, D., & Denčić-Mihajlov, K. (2014). Transparency of financial reporting in Serbia–regulatory framework and reporting practices. Procedia Economics and Finance, 9, 153-162.Available at: https://doi.org/10.1016/s2212-5671(14)00016-1.

Tambun, S., & Haryati, A. (2022). The influence of nationalism’s attitude and tax morals on taxpayer compliance through tax awareness. Journal of Accounting, Business and Finance Research, 14(1), 1–7.Available at: https://doi.org/10.20448/2002.141.1.7.

Wibowo, A., & Darmanto, S. (2017). Reaction of Indonesian capital market investors to the implementation of tax amnesty. Journal of Finance and Banking, 21(40), 597-608.