Tax Compliance Model Based on Planned Behavior of Taxpayers Mediating Intention to Pay Taxes

Markonah Markonah1*

Sumarno Manrejo2

1Economics and Business Faculty, Perbanas Institute, Jakarta, Indonesia. 2Economics and Business Faculty, Bhayangkara University, Jakarta, Indonesia. |

AbstractThe main purpose of this research is to investigate a tax compliance model in which taxpayers' planned behavior mediates their intention to pay taxes, in order to provide strategic policy recommendations to the government and strengthen the implementation of the self-assessment system in Indonesia. The population used in this research comprised those taxpayers who reported their annual tax returns in Jakarta and West Java in the 2021 fiscal year. A sample of 229 respondents was selected using a purposive sampling method. The data were processed using Lisrel 8.80. This research combines quantitative and qualitative methods (mixed-method) and supplements the sample data with information gained from in-depth interviews and focus group discussions with relevant departments at the Directorate General of Taxes of the Republic of Indonesia as well as various experts in their fields, thereby strengthening the justification of the research results. The results show that taxpayers’ planned behavior has no direct effect on tax compliance, though it does mediate the intention to pay taxes. Taxpayers’ planned behavior thus affects tax compliance via the intention to pay taxes. Thus it is recommended that the government fosters taxpayers' intention to pay taxes through socialization, education, and continuous law enforcement to create a sense of justice in the community. |

Licensed: |

|

Keywords: JEL Classification |

|

Received: 21 January 2021 |

Funding: This study received no specific financial support. |

Competing Interests: The authors declare that they have no competing interests. |

1. Introduction

Countries around the world need considerable funds to run their government (OECD, 2019). Taxes are usually the biggest contributor to a country’s revenue, so tax compliance is necessary. However, many compliance issues arise in every country, including Indonesia, possibly because taxpayers try to be efficient, and the government struggles to meet its revenue targets, even as the target continues to increase every year. The data shows that in the last ten years, Indonesia has not been able to meet its tax revenue target (Ministry of Finance, 2019). This situation has caused Indonesia’s tax ratio to be as low as 11.7 percent in 2019. Moreover, the Ministry of Finance Performance Report reveals that this condition was exacerbated by the Covid-19 pandemic (Nasution, Erlina, & Muda, 2020).

Indonesia’s low tax ratio indicates that tax revenue is less than optimal due to the low level of tax compliance. Taxpayer compliance is manifested in both periodic and annual tax returns, which are the mainstays of the self-assessment system (Pham, Le, Truong, & Tran, 2020). Tax compliance is closely related to taxpayer behavior (Caspers, 2020).

Indonesia’s tax compliance is relatively low, as is clear from the fact that the projected tax revenues in the Republic of Indonesia’s State Revenue and Expenditure Budget have not been achieved in the last ten years (Ministry of Finance Performance Report, 2019). In fact, Indonesia’s revenue from the tax sector is around 85 percent (Ministry of Finance, 2019).

Indonesia is classified as a country with a low tax ratio, meaning that the tax revenues collected by the Indonesian government are less than optimal (Novianti & Dewi, 2018). To conduct research related to tax compliance it is necessary to consider the taxpayers’ behavior, including their planned behavior, by refining the theory of taxpayer planned behavior, for example, the intention to pay taxes as a form of tax compliance, in the context of a broader understanding of human behavior (Otieno, Liyayla, & Odongo, 2015). Taxpayers’ behavior includes their intention to make tax payments, which has an impact on tax compliance behavior (Novianti & Dewi, 2018). Taxpayers’ attitudes, subjective norms, and perceived behavior control can affect their intention to pay taxes, which significantly affects tax compliance behavior. The results of Smart (2013) revealed that taxpayer compliance can be influenced by behavioral attitudes, subjective norms, and perceptions of behavior control; taxpayers’ actions and behavioral intentions to pay taxes have a positive impact on tax compliance. The tax office can influence behavioral intentions, although tax compliance behavior can also be affected by many other factors, especially factors inherent in the taxpayers themselves (Salman & Sarjono, 2013). The research conducted by Novianti and Dewi (2018) concluded that subjective attitudes and norms in the planned behavior of taxpayers have a significant impact on their intention to pay taxes.

The current study aims to produce a tax compliance model based on taxpayers’ planned behavior mediated by their intention to pay taxes. Conceptual models and empirical studies are used to provide strategic recommendations for policies and regulations that support the implementation of a self-assessment system. Such research has not previously been carried out in Indonesia, and this gap, combined with Indonesia’s low tax compliance, was the motivation for this research.

2. Literature Review

2.1. Tax Compliance

Based on Law Number 16 of 2009 concerning General Provisions and Tax Procedures Article 17C paragraph (2), what is meant by taxpayers’ compliance is whether they meet the following criteria: (a) submitting tax returns on time; (b) no tax arrears for any type of tax, except where tax arrears result from having obtained permission to pay in installments or defer tax payments; (c) financial statements are audited by a public accountant or government financial supervisory agency with an unqualified opinion for three consecutive years; (d) never having been convicted of an offense in the field of taxation based on a court decision that has permanent legal force for a five-year period. This strengthens PMK Number 74/PMK.03/2012 concerning the procedures for determining taxpayers with certain criteria in order to pre-refund tax overpayments (Minister of Finance Regulation, 2018).

2.2. Intention to Pay Tax

According to Novianti and Dewi (2018), intention is something that inclines someone to perform a certain behavior or automatically determines someone’s actions. This is in line with Pahlsson (2017), who stated that tax law includes references to taxpayers’ intentions or resolutions to pay taxes on their transactions. Intention to pay taxes means that taxpayers are ready to pay those taxes and fulfill all their tax obligations (Dobos & Takács-György, 2020; Tambun & Haryati, 2022). The taxpayer’s intention to pay taxes is the key to tax compliance. Intention plays a crucial role in explaining a citizen’s obedient or disobedient behavior regarding tax payment. In this research, intention to pay taxes is considered a behavior that is influenced by the planned behavior of taxpayers, which could affect tax compliance. Furthermore, it has been emphasized that a taxpayer’s intention to pay taxes is the key to taxpayer compliance. An indication of the intention to pay taxes, such as if the taxpayer tends to pay taxes, attempts to pay taxes, or decides to pay taxes, can help ascertain the level of tax payments that will enter the state treasury (Minister of Finance Regulation, 2018).

2.3. Taxpayer Planned Behavior

A taxpayer’s planned behavior in this research can be defined as an individual forming a clear intention to exhibit tax-compliant behavior. Taxpayers’ planned behavior comprises three behavioral components: attitudes, subjective norms, and perceived behavioral control. Based on these components, seven determinants were developed to examine tax compliance intentions: tax morale, tax fairness, trust in government, perceived power of authorities, tax complexity, tax information, and tax awareness (Taing & Chang, 2021). Subjective norms refers to the views of certain people that are relevant to the individual who performs the behavior and which are often used as guidelines about the acceptability of the behavior. Attitude requires the person who performs the behavior to assess their beliefs relative to their actions (Caspers, 2020). The neoclassical economic view that applies to tax behavior research is that trust is good, but control is better (Kirchler, Kogler, & Muehlbacher, 2014).

2.4. The Theory of Planned Behavior

In the Theory of Planned Behavior, there are seven determining factors, namely: tax morale, tax justice, trust in the government, perceived power of authorities, tax complexity, tax information, and tax awareness. Of these seven factors, some influence tax compliance, but others do not (Taing & Chang, 2021). This finding strengthens the Theory of Planned Behavior, which states that a person's attitude toward an object and their subjective norms will affect the person's behavior through their intentions (Salman & Sarjono, 2013).

2.5. Previous Research

Taing and Chang (2021) defined taxpayers' planned behavior as consisting of seven determinants, which they developed to analyze tax compliance intentions; these were: tax morale, tax justice, trust in the government, perceived power of authorities, tax complexity, tax information, and tax awareness. Tax morale, tax justice, and tax complexity were confirmed to have a statistically significant effect on citizens' tax compliance intentions, while the power of authority, trust in government, tax information, and tax awareness had no significant effect. According to Saputra (2019), the results of this hypothesis examination indicate that perceived attitudes and behavioral control have a positive and significant effect on tax compliance intentions, while subjective norms do not affect tax compliance intentions. The results of Pratami, Sulindawati, and Wahyuni (2017) study showed that attitude has a positive and significant effect on personal taxpayer compliance, and intention to pay taxes also has a positive and significant effect on personal taxpayer compliance. Furthermore, the results of Suyono (2016) indicate that taxpayers’ behavior has a positive effect on tax compliance, and the intention to pay taxes has a significant positive effect on tax compliance as well. Ali and Nasaruddin (2020) showed that taxpayers’ behavior, tax services, and tax audits have a significant positive effect on willingness to pay taxes at West Makassar's KPP Pratama. According to Syakura and Ginting (2017), taxpayer behavior and intention to use e-filing both have a significant positive effect on tax compliance. Taxpayers’ behavior also has a significant positive effect on their intention to use e-filing. Likewise, Maryani (2019) stated that taxpayer behavior has a significant positive effect on tax compliance.

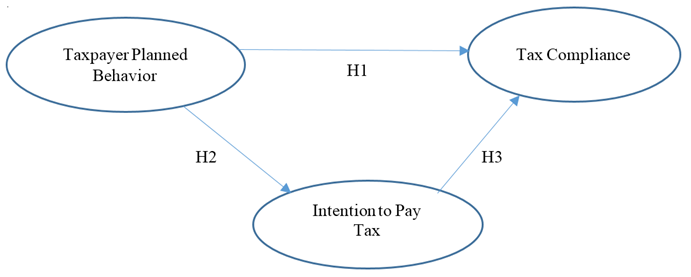

2.6. Conceptual Framework

The study’s conceptual framework is based on Big Theory, Intermediate Theory, and Applied Theory, which were used to form the constructs and dimensions of the conceptual framework that serves as a roadmap for the research (Adom, Hussein, & Agyem, 2018). Research by Suyono (2016) shows that taxpayer behavior and intention to pay taxes have a positive impact on tax compliance.

Pratami et al. (2017) found that the attitude toward and intention to pay taxes had the effect of increasing individual taxpayer compliance. Tax regulations are very complex and even tend to change from time to time, yet taxpayers are required to understand and implement them. This complexity affects the level of taxpayer compliance as well as the implementation of the self-assessment system in Indonesia (Hutauruk et al., 2019); (Minister of Finance Regulation, 2018). The conceptual framework of the research is shown in Figure 1.

Figure 1. The study’s conceptual framework.

2.7. Hypotheses

Based on Figure 1, the proposed hypotheses can be stated as follows:

H1: Taxpayer Planned Behavior has a significant positive effect on Tax Compliance.

H2: Taxpayer Planned Behavior has a significant positive effect on Intention to Pay Taxes.

H3: Intention to Pay Taxes has a significant positive effect on Tax Compliance.

H4: Intention to Pay Taxes could mediate the effect of Taxpayer Planned Behavior on Tax Compliance.

2.8. State of the Art

The main contribution of this research, or its “State of the Art” or novelty value, lies in its investigation of the mediating effect of the intention to pay taxes on the relationship between taxpayers’ planned behavior and their tax compliance, an effect that has not been previously studied.

3. Research Methods

The population of this research consists of individual taxpayers who submitted their 2021 annual tax returns in Jakarta and several other cities in West Java, Indonesia – a total of 12,054,209 taxpayers. The sample used was 229 respondents who were recruited through a purposive sampling technique (Sugiyono, 2016). Multivariate statistical analysis was carried out, and the data was processed using Lisrel 8.80; this included identifying endogenous and exogenous latent variables, constructing path diagrams, formulating equations, identifying models, examining their goodness of fit, and interpreting the models (Hair, Black, Babin, & Anderson, 2018).

The type of data utilized was primary data obtained from the Directorate of P2 Public Relations of the Director of Taxes, as well as data obtained directly from taxpayers. The latter data were collected using a questionnaire measured on a Likert scale with values ranging from 1 to 5. To strengthen the analysis results, interviews were conducted with several directors of intelligence, the Director of P2 Public Relations, and the Director of International Taxation at the Directorate General of Taxes of the Republic of Indonesia (Sekaran & Bougie, 2016).

This research used a mixed methodology that combines quantitative and qualitative research (Hussain, Fangwei, Siddiqi, Ali, & Shabbir, 2018). The strategy used in mixed method research is the concurrent triangulation of questionnaire, interview, and tax information to collect both qualitative and quantitative data and then compare the two (Hair et al., 2018).

4. Results and Discussion

The results of the study’s statistical tests, which are reported in Table 1, indicate that:

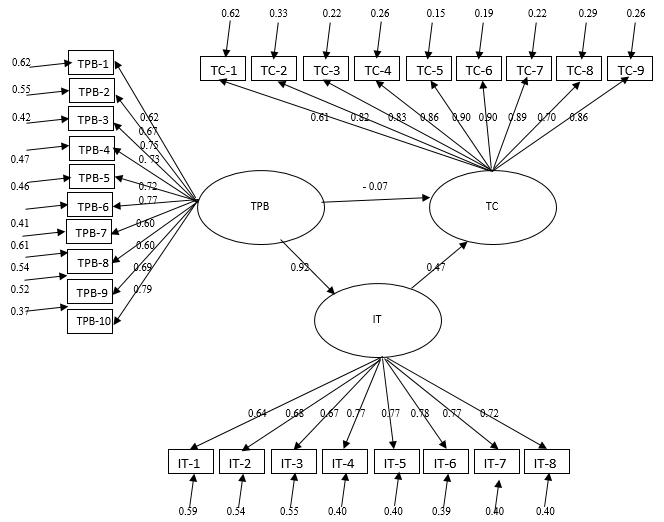

- Taxpayers’ planned behavior has no significant negative effect on tax compliance. This is shown by the coefficient value of -0.07 and t-value (0.35) < 1.97, meaning that H1 was rejected.

- Taxpayers’ planned behavior has a significant positive effect on the intention to pay taxes. This is shown by the coefficient value of 0.92 and t-value (10.00) > 1.97, meaning that H2 was accepted.

- Intention to pay taxes has a significant positive effect on tax compliance. This is shown by the coefficient value of 0.47 and t-value (2.75) > 1.97, meaning that H3 was accepted.

- Intention to pay taxes mediates the effect of taxpayer behavior planning on tax compliance. This is shown by the coefficient value of 0.43 and t-value (27.50) > 1.97, meaning that H4 was accepted.

| Hypothesis | Path | t-value |

Coefficient |

Result |

| H1 | Taxpayer planned behavior (TPB) à Tax compliance (TC) | -0.35 |

-0.07 |

Rejected |

| H2 | Taxpayer planned behavior (TPB) à Intention to pay tax (IT) | 10.00 |

0.92 |

Accepted |

| H3 | Intention to pay tax (IT) à Tax compliance (TC) | 2.75 |

0.47 |

Accepted |

| H4 | Taxpayer planned behavior (TPB) à Intention to pay tax (IT) à Tax compliance (TC) | 27.50 |

043 |

Accepted |

According to the statistical test results, taxpayers’ planned behavior has an insignificant negative effect on tax compliance. This proves that tax compliance is a complex issue that cannot be created directly, though it can be influenced by environmental conditions that help determine taxpayers’ decisions. This condition is likely related to the implementation of the self-assessment system in Indonesia, which means that taxpayers, in an effort to reduce tax costs, carry out various tax planning strategies. Basically, the purpose of implementing the self-assessment system is to grant taxpayers the confidence to be more independent in managing their own tax administration. This tax collection strategy was adopted in Indonesia to build a modern taxation system, based on the principle of full delegation of trust to taxpayers. The success of this strategy requires awareness, honesty, and discipline on the part of taxpayers when carrying out their tax obligations so that they fulfill both the material and formal aspects of their tax obligations. This result represents the first novelty of the current study because it has not been found in prior research.

The self-assessment system allows taxpayers to conduct tax planning to minimize their costs using various possible strategies without having to violate tax rules – known as tax avoidance. However, there is the possibility of tax evasion if it is more profitable than tax planning. Taxpayers, in calculating the tax they owe, need to consider the fiscal provisions regulated by Law Number 36 of 2008 concerning Income Tax, especially Article 6, which regulates fiscal costs, and Article 9, which states that costs cannot be financed fiscally. Income tax is a type of cost that is commercially financed, but the opposite treatment cannot be financed fiscally, therefore taxpayers can work around this using several strategies, such as maximizing deductible expenses using the gross-up method, delaying income, accelerating the assignment of costs, and other strategies (Pohan, 2018). The results of this research can also be interpreted to mean that the more taxpayers plan their behavior, the more taxpayer compliance decreases and vice versa. This is due to the very heterogeneous behavior of taxpayers: some are obedient, some try to comply, some are unintentionally disobedient, and some are deliberately disobedient. Taxpayers can perform tax planning to improve efficiency because the tax system in Indonesia is based on self-assessment, which gives taxpayers full authority to calculate their taxes independently. The results of this study are in line with those of Saputra (2019). Researching social norms more comprehensively, the results show that the taxpayers’ planned behavior has a significant effect on tax compliance. These results were strengthened by the results of the interviews. However, it contradicts the results of Suyono (2016) and Pratami et al. (2017), who declared that the level of tax compliance was determined by many factors, especially the taxpayers’ behavior, whereas in Indonesia the level of taxpayer compliance is still low.

According to the statistical test results, the taxpayer's planned behavior has a significant positive effect on the intention to pay taxes. This means that taxpayers who have well-planned behavior tend to have the intention to pay their taxes. Taxpayers’ planned behavior has a significant positive effect on the intention to pay taxes, according to research by Saputra (2019) and Suyono (2016). Taxpayers are compliant about paying taxes if their rights are fulfilled or their contra-achievements can be fulfilled by the government so that they feel the benefits of paying taxes, therefore they are commensurate with the sacrifices that have been made; this is in accordance with justice theory. Public trust in the government will increase if the public’s perception of the tax system implemented by the government is that it is fair and beneficial from a procedural, distributive and retributive perspective.

Based on the statistical test results, the intention to pay taxes has a significant positive impact on tax compliance. This means that taxpayers who intend to pay taxes tend to display tax compliance. The taxpayer’s intention to pay taxes is the key to tax compliance; even when the amount of tax owed has been calculated, if there is no intention to pay taxes, the tax will not go to the state treasury. Intention to pay taxes has a central role in explaining the behavior of an individual who is compliant or non-compliant in paying taxes. The most dominant indicators that reflect the intention to pay taxes are trying to correctly comply with paying taxes and self-awareness about paying taxes. This can be interpreted to mean that paying taxes correctly with self-awareness is the correct outcome of self-assessment and is a prerequisite for obedient taxpayers. Intention to pay taxes has a significant positive effect on tax compliance. This means that the greater the taxpayers’ planned behavior, the more taxpayer compliance will increase. The research results are in line with Taing and Chang (2021) with regard to the theory of planned behavior, which describes how attitudes, norms, and perceived intentional behavior have a significant effect on tax compliance.

Figure 2. Structural standardized full model.

Based on the statistical test results, taxpayers planned behavior has a significant positive mediating effect on the relationship between intention to pay taxes and tax compliance. This can be interpreted to mean that the better the planned behavior and the stronger the intention of the taxpayer to pay taxes, the higher the level of taxpayer compliance will be. This result is the central point of this research and represents the second novel finding of this study, as it has not been found in any previous research. However, the result is in accordance with the theory that humans are rational beings and use good information to achieve their goals. Citizens think about the implications of their actions before they decide to take or avoid taking certain actions, including, in this case, the taxpayer deciding to pay their taxes or delay, or even, under certain circumstances, choosing not to pay their owed taxes (tax evasion). Efforts by taxpayers to optimize benefits and reduce fiscal costs are known as tax planning. Taxpayers can take this action because of the self-assessment system implemented in Indonesia. The mediating effect of taxpayers’ planned behavior on the relationship between the intention to pay taxes and tax compliance is strong (fully mediating), meaning that the exogenous variable of the taxpayer’s planned behavior, by mediating the variable intention to pay taxes, is able to affect tax compliance. The taxpayer’s decision to comply with taxes depends on the taxpayer’s intention to pay taxes; the higher the level of the taxpayer’s planned behavior, the higher the tax compliance will be, by mediating the intention to pay taxes. The increase in tax compliance will ensure increased tax revenues for the state so that Indonesia’s tax ratio will increase. The increase in tax compliance, which is strengthened by taxpayers’ intention to pay taxes, is both a form of awareness on the part of the taxpayers and a form of compliance with the self-assessment system in Indonesia.

The results of this research reveal that taxpayers’ planned behavior fully mediates the intention to pay taxes because the analysis of the taxpayers’ planned behavior showed that it cannot directly affect tax compliance, but by mediating the intention to pay taxes, there is a significant positive effect on tax compliance. The increase in tax compliance is expected to increase state revenues. If tax revenues increase, Indonesia’s tax ratio will also automatically increase, allowing it to catch up with other countries, particularly developed countries with high tax ratios. Figure 2 illustrates the structural standardized full model.

5. Conclusion

The results of this research have revealed that taxpayers’ planned behavior has no direct effect on tax compliance, but does mediate the intention to pay taxes, which has a significant positive effect on tax compliance in Jakarta and West Java. Based on the test results, data analysis, and discussion that has been presented above, the following conclusions can be drawn:

1) The taxpayer's planned behavior has no direct effect on tax compliance. In short, taxpayers are not willing to pay taxes because they do not receive a direct contra-achievement. In this case, the government must force taxpayers through tax laws and regulations. The results of this research thus indicate that tax compliance cannot be directly influenced by taxpayers’ planned behavior.

2)The taxpayer's planned behavior has a significant positive effect on their intention to pay taxes. The taxpayers' planned behavior is a variable that affects the intention to pay taxes, and the intention to pay taxes is strongly influenced by the taxpayers' planned behavior. The taxpayers’ planned behavior can change at any time so it must be built early or be influenced by trusted people around them.

3) Intention to pay taxes has a significant positive effect on tax compliance. Tax compliance is influenced by the intention to pay the tax itself. Tax compliance will thus be achieved if the taxpayer has the intention to pay taxes.

4) The intention to pay taxes fully mediates the effect of the taxpayer's planned behavior on tax compliance. Tax compliance is influenced by the taxpayer’s planned behavior through the intention to pay taxes. The taxpayer's planned behavior has not been proven to directly affect tax compliance, the results showed an insignificant negative effect, so it needs to be mediated by the intention to pay taxes to achieve tax compliance. This relates to human nature, as taxpayers naturally object to paying taxes because the tax payments made are not rewarded with a direct contra-achievement; for taxpayers to comply with paying taxes, they must be forced by government regulations. The taxpayers’ planned behavior, by mediating their intention to pay taxes, has a significant positive effect on tax compliance.

Certain strategic recommendations can be made to the Directorate General of Taxes of the Republic of Indonesia, the holder of the tax authority, to improve taxpayer compliance:

1) The government must strengthen citizens’ intention to pay taxes through continuous socialization, education, and law enforcement to create a sense of justice in the community.

2) The government should make the process easier for taxpayers. By making paying taxes as easy as buying credit via an ATM, improved services are provided to taxpayers, which will improve tax compliance and thus increase tax revenue to meet the targets set by the government. This will increase the independence of a sovereign state by negating dependence on loans from other countries.

The implementation of the self-assessment system by the government requires taxpayers to display greater responsibility in terms of calculating, depositing, and reporting. By being tax-compliant, taxpayers can obtain optimal benefits and reduce costs efficiently to achieve the goals that have been set because, through tax compliance, taxpayers can avoid the imposition of taxation sanctions in the form of interest, fines, and increases. Because the intention to pay taxes is fully mediated by the impact of taxpayers’ planned behavior on tax compliance, the government needs to increase the intention to pay taxes by educating the public and improving their planned behavior.

References

Adom, D., Hussein, E. K., & Agyem, J. A. (2018). Theoretical and conceptual framework: Mandatory ingredients of a quality research. International Journal of Scientific Research, 7(1), 438-441.

Ali, I., & Nasaruddin, F. (2020). Several factors influence the willingness to Pay taxes. Point of View Research Accounting and Auditing, 1(3), 57-70.Available at: https://doi.org/10.47090/povraa.v1i3.41.

Caspers, C. G. (2020). Role of trust in adopting consumer social responsible behaviour in the context of water use in domestic households. The South East European Journal of Economics and Business, 15(1), 1-13.Available at: https://doi.org/10.2478/jeb-2020-0001.

Dobos, P., & Takács-György, K. (2020). The impact of the relationship between the state, state institutions and tax payers on willingness to pay tax. Serbian Journal of Management, 15(1), 69-80.Available at: https://doi.org/10.5937/sjm15-21750.

Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2018). Multivariate data analysis (8th ed.). Hampshire: Cengage Learning.

Hussain, S., Fangwei, Z., Siddiqi, A. F., Ali, Z., & Shabbir, M. S. (2018). Structural equation model for evaluating factors affecting quality of social infrastructure projects. Sustainability, 10(5), 1415.Available at: https://doi.org/10.3390/su10051415.

Hutauruk, M. R., Ghozali, I., Sutarmo, Y., Mushofa, A., Suyanto, M., Yulidar, A., & Yanuarta, W. (2019). The impact of self-assessment system on tax payment through tax control as moderation variables. International Journal of Scientific and Technology Research, 8(12), 3255-3260.

Kirchler, E., Kogler, C., & Muehlbacher, S. (2014). Cooperative tax compliance: From deterrence to deference. Current Directions in Psychological Science, 23(2), 87-92.Available at: https://doi.org/10.1177/0963721413516975.

Maryani, N. K. J. (2019). The impact of taxpayer behavior on taxpayer compliance through the use of E-filing as an intervening variable at KPP Pratama Gianyar. Journal of Science, Accounting and Management, 1(2), 107-150.

Minister of Finance Regulation. (2018). PMK No. 39/PMK.03/2018 concerning criteria for compliant taxpayers. Ministry of Finance of the Republic of Indonesia.Retrieved from: https://perpajakan-id.ddtc.co.id/sumber-hukum/peraturan-pusat/peraturan-menteri-keuangan-39pmk-032018.

Ministry of Finance. (2019). Our state budget January 2019 Edition. Ministry of Finance of the Republic of Indonesia. Retrieved from https://www.kemenkeu.go.id/media/11647/apbn-kita-edisi-januari-2019.pdf .

Ministry of Finance Performance Report. (2019). The ministry of finance's 2019 performance report, a resilient Indonesian economy. Ministry of Finance of the Republic of Indonesia. Retrieved from https://www.kemenkeu.go.id/media/17022/laporan-tahunan-kementerian-keuangan-2019.pdf .

Nasution, D. A. D., Erlina, E., & Muda, I. (2020). The impact of the Covid-19 pandemic on the Indonesian economy. Journal of Benefits, 5(2), 212-224.

Novianti, A. F., & Dewi, N. H. U. (2018). An investigation of the theory of planned behavior and the role of tax amnesty in tax compliance. The Indonesian Accounting Review, 7(1), 79-94.Available at: https://doi.org/10.14414/tiar.v7i1.961.

OECD. (2019). Revenue statistics in Asian and pacific economies 2019. Organisation for Economic Co-Operatuin and Development. Retrieved from https://www.oecd.org/tax/tax-policy/revenue-statistics-in-asia-and-the-pacific-5902c320-en.htm .

Otieno, O. C., Liyayla, S., & Odongo, B. C. (2015). Theoretical and practical implications of applying theory of reasoned action in an information systems study. Open Access Library Journal, 2, e2054.Available at: https://doi.org/10.4236/oalib.1102054.

Pahlsson, R. (2017). The taxpayer’s intentions: Subjective prerequisites in tax law. Nordic Tax Journal, 2017(1), 121-134.Available at: https://doi.org/10.1515/ntaxj-2017-0009.

Pham, T. M. L., Le, T. T., Truong, T. H. L., & Tran, M. D. (2020). Determinants influencing tax compliance: The case of Vietnam. The Journal of Asian Finance, Economics and Business, 7(2), 65-73.Available at: https://doi.org/10.13106/jafeb.2020.vol7.no2.65.

Pohan, C. A. (2018). The complete guide to international taxes. Jakarta: Gramedia Pustaka Utama.

Pratami, L. P. K. A. W., Sulindawati, N. L. G. E., & Wahyuni, M. A. (2017). The effect of the implementation of the taxation e-system on the level of compliance of individual taxpayers in paying taxes at the tax service office (KPP) Pratama Singaraja. JIMAT (Accounting Student Scientific Journal) Undiksha, 7(1), 104.

Salman, K. R., & Sarjono, B. (2013). Intention and behavior of tax payment compliance by the individual tax payers listed in Pratama tax office West Sidoarjo Regency. Journal of Economics, Business, & Accountancy VENTURA, 16(2), 309-324.Available at: https://doi.org/10.14414/jebav.v16i2.188.

Saputra, H. (2019). Analysis of tax compliance with theory of planned behavior (Against Individual Taxpayers in DKI Jakarta Province). Muara Journal of Economics and Business, 3(1), 47-58.

Sekaran, U., & Bougie, R. (2016). Research methods for business: A skill building approach. Chichester: John Wiley & Sons.

Smart, M. (2013). Applying the theory of planned behaviour and structural equation modelling to tax compliance behaviour: A New Zealand study. New Zealand: University of Canterbury.

Sugiyono, S. (2016). Combination research methods (Mixed Method). Jakarta: Alfabeta.

Suyono, N. A. (2016). Factors affecting compliance in paying taxes at the Wonosobo tax office. Journal of Research and Community Service UNSIQ, 3(1), 1-10.

Syakura, M. A., & Ginting, Y. L. (2017). Analysis of taxpayer behavior on intention to Use E-filling and taxpayer compliance (Study on Taxpayers with Profession as Lecturer). AKUNTABEL, 14(1), 46-56.

Taing, H. B., & Chang, Y. (2021). Determinants of tax compliance intention: Focus on the theory of planned behavior. International Journal of Public Administration, 44(1), 62-73.Available at: https://doi.org/10.1080/01900692.2020.1728313.

Tambun, S., & Haryati, A. (2022). The influence of nationalism’s attitude and tax morals on taxpayer compliance through tax awareness. Journal of Accounting, Business and Finance Research, 14(1), 1–7.Available at: https://doi.org/10.20448/2002.141.1.7.