Do Industry-Wise Investment Returns Influence the Aggregate Investment Returns of CPSEs in India?

Sudipta Ghosh1*

P.S. Aithal2

1Post-Doctoral Research Fellow of Srinivas University, Mangalore, India; Faculty of Commerce, Prabhat Kumar College, Contai, W.B., India. |

AbstractThe term “investment return” may be defined as a gauge used to calculate the efficiency or profitability of an investment. It also helps to assess the effectiveness of different investments at a certain point in time. In this context, the focal objective of the study is to examine whether industry-wise investment returns influence aggregate investment returns of Central Public Sector Enterprises (CPSEs) in India during the period 2010-2011 to 2019-2020. The study concerns all the in-service CPSEs in India, aside from public enterprises that run departmentally, indemnity companies, and banking organizations. Moreover, the selected sample is classified into 20 different industries, including 13 industries within the manufacturing sector and 7 industries within the service sector. The findings of the study reveal that few industries positively drive the performance of CPSEs’ aggregate investment returns. Hence, the performance of aggregate CPSEs in terms of investment returns is mainly driven by the performance of COI, OMMI, SI, TVEI, ICGI, PGI, CCTCSI, and FSI. In terms of overall profitability (i.e., ROCE), PGI has the highest positive influence (0.85), while ICGI has the lowest positive influence (0.04) on the overall profitability of the aggregate CPSEs – values which are found to be significant at the 5% level. |

Licensed: |

|

Keywords: |

|

Received: 2 March 2022 |

|

| (* Corresponding Author) |

Funding: This study received no specific financial support. |

Competing Interests:The authors declare that they have no competing interests. |

1. Introduction

The term “investment return” (popularly called Return on Investment or ROI) may be defined as a performance measure used to calculate the effectiveness of an investment. It also helps assess the effectiveness of different investments at a certain point in time. ROI is an attempt to straightforwardly gauge the return of a particular investment in relation to its investment cost.

Thus, ROI = Investment Benefit / Investment Cost. The resultant figure is articulated as a relative amount or percentage.

In the literature on financial management, investment returns are measured using the following popular investment ratios (Khan & Jain, 1994):

- ROA: This ratio measures how much return (i.e., profit) is generated from the total assets employed in the business.

- ROCE: This indicates the return in relation to the long-term funds provided by the owners and long-term creditors.

- ROE: This ratio measures the return for a company’s equity shareholders.

2. Central Public Sector Enterprises (CPSEs) in India: A Synoptic Overview

CPSEs in India have been established to serve the wide macroeconomic objectives of economic growth, self-reliance in production, excess balance of payments, and controlling inflationary and deflationary trends. They are viewed as a device to bring about structural transformation of the economy with fairness and social justice.

In the First Five Year Plan, there were only 5 CPSEs with a total capital outlay of Rs. 29 crore, while as of 31st March 2019 there are 348 CPSEs with a total outlay of Rs. 16,40,628 crore. The CPSEs are regarded as strategic players in the building of an economy. They provide necessary goods and services and occupy a significant market position in vital sectors like petroleum, coal, electricity, steel, mining, transport, and logistic services. The CPSEs also operate in cutthroat markets like telecommunications, information technology, hospitality, etc.

3. Literature Review

Sankar and Reddy (1989) stated that state-owned PSEs could be considered high or low based on three factors, i.e., their social purpose, profitability, and resource collection. The study observed that state-owned PSEs that operate in a competitive market with a low social purpose and low resource collection were the most appropriate players for disinvestment.

Antony (1992) examined the effectiveness of the CPSEs in Kerala in terms of facility exploitation, profitability, and productivity. The study observed a declining trend in the investment pattern of the CPSEs in Kerala with a low level of capacity utilization. Due to the low level of capacity utilization, the CPSEs in Kerala incurred huge production losses. In terms of profitability, the study indicated that the profitability of the enterprises could be improved by raising capacity utilization. In terms of productivity, the study concluded that despite the increase in labor productivity, capital productivity had reduced to some extent.

On the whole, the study concluded that the reform measures adopted within the public enterprises and among the ministers and in other related government agencies had brought the desired results to the CPSEs. The study further suggested that privatization is a short-term measure rather than a long-term measure for achieving efficiency. Galal (1994) attempted to determine whether the process of privatization augmented the efficiency of twelve companies in selected countries. The study indicated that privatization cannot be held responsible for all the troubles associated with the transition. Further, a study of the financial performance revealed enhanced profitability and sales efficiency. Megginson and Netter (2001) reviewed the various aspects of privatization, comparative performance between public sector and private sector companies, types of privatization, the effect of privatization on the growth of capital markets, etc. The study observed that privatized companies became more competent and achieved better financial health.

Ray and Maharana (2002) evaluated the disinvestment of PSEs in India from 1991 to 2001. The results showed that the disinvestment of PSEs had a small effect during the period under study. The study recommended that the numerous criticisms and controversies against disinvestment be addressed through increased transparency. Patnaik (2007) concluded that the main goal of disinvestment is to improve the efficiency in the use of a country’s labor and wealth. The study revealed that limited privatization and government control produced higher outputs. The study suggested that the public should be offered shares during the process of disinvestment of profit-making enterprises since it would avoid the concentration of economic power. Gagan Singh and Paliwal (2010) attempted to empirically examine the impact of disinvestment on the monetary and operating performance of Indian public sector companies during the period 1985-86 to 2004-05. The study employed statistical tests to analyze data collected from the audited reports of Indian PSEs and records of the Govt. of India. The study results showed that the operating performance of the competitive firms declined after disinvestment, in terms of sales and profitability, while the monopoly firms were found to be efficient in terms of profit.

Rastogi and Shukla (2013) examined the challenges and effects of disinvestment on the Indian economy. The findings of the study indicated that disinvestment did not produce satisfactory results, which may be due to various reasons like high costs, operational inefficiency, excessive government interference, etc. The study recommended that the government. should target strategic disinvestment. The study concluded that the government should take the necessary steps to improve the efficiency of inefficient units, and a competitive market should be developed so that the PSEs can work efficiently to better the economy. Singh (2015) carried out a study on the CPSEs in India. The study results found that the process of disinvestment had improved the profitability of the CPSEs that incurred losses before disinvestment. The researcher also suggested that equity shares must be given to the employees of the profit-making CPSEs as well as the public. Disinvestment could lead to increased efficiency in the functioning of the CPSEs, but irresponsible privatization may not lead to positive results for the CPSEs in the long term. The study noted that the government should seriously consider the suggestions of the Rangarajan Committee on privatization.

Cadoret (2016) attempted to evaluate the impact of return on investment on investment expenditures through budgetary slacks. The study did not find any probable relationship between ROI and budgetary slacks. Nevertheless, the study observed that slacks could be highly influenced by project size. The researcher suggested that ROI was not a good technique for controlling investment expenditures. Sharma (2016) attempted to evaluate the impact of disinvestment on the financial performance of public sector enterprises in India. The study concluded that public sector enterprises performed better in the post-reform period (i.e., after disinvestment). The public sector enterprises achieved better performance due to high productivity and reduced production costs.

George and Vinod (2016) carried out a study on the performance of CPSEs in India for the period 2004-2015. The study observed that the turnover of the CPSEs increased up to 2012 and net profit increased at a declining rate up to 2014. The expansion velocity of CPSEs that incurred losses augmented at an increasing rate, while the expansion velocity of the CPSEs that incurred profits increased at a decreasing rate. The study further observed a negative annual growth rate in return on capital employed which revealed a lack of efficiency in the working of the CPSEs.

Singh (2017) concluded that despite various initiatives being adopted to improve the financial performance of CPSEs in India, policymakers still face a big challenge to improve the competitiveness and efficiency of the CPSEs. The study further observed that the reform measures adopted so far had a positive effect on the performance of CPSEs in India. Mandiratta and Bhalla (2017) investigated the monetary and working performance of fifteen CPSEs that were disinvested in India in the period 2003–2012. The sample of the study represented four cognate groups, i.e., the manufacturing, mining, energy, and service sectors. Ratio analysis and panel data estimation techniques were used in the study. The researchers observed a significant increase in overall operational competence in terms of sales and net earnings effectiveness, whereas insignificant results were observed in the area of profitability.

Kumar (2017) strategically analyzed the disinvestment of public sector units in India. The study stated that disinvestment was very important to make PSEs more efficient and collect funds to reduce the fiscal deficit. In India, the disinvestment process was confronted with several problems. Hence, the study suggested that the government should make the disinvestment process more transparent and introduce the concept of corporate governance. The study further suggested that proper steps should be taken by the government to create and sustain a competitive capital market and to implement the required legal reforms.

Achini and Begum (2018) examined and compared the impact of disinvestment on the fiscal performance of selected Maharatna and Navratna companies. A paired t-test was applied to measure this impact during the period 2007 to 2017, with the year 2012 being considered the base year. The result of the study indicated that Maharatna companies experienced a significant impact, while no significant impact of disinvestment was found in the Navratna companies. Batth, Nayak, and Pasumarti (2018) carried out a study on the financial performance of Indian public sector undertakings using the Altman Z score model technique for the period 2011-12 to 2015-16. The study considered companies that belonged to the Maharatna and Navratna categories. The study found that 13 companies had good financial performance, while 9 companies had poor financial health. The remaining 2 companies showed less market capitalization during the study period. An important observation of the study was that companies with a sound financial position had less market capitalization.

Ghosh (2019a) assessed the performance of CPSEs through inventory management based on secondary data during the period 2000-01 to 2016-17. Popular inventory ratios were used, and linear regression equations were applied to derive the findings of the study. The study found that inventory ratios showed better performance up to 2008-09. Moreover, there were no significant deviations between actual values and trend values of inventory turnover ratio. On the whole, the researcher concluded that inventory management of Indian CPSEs was satisfactory during the period under study.

Ghosh (2019b) attempted to compare the liquidity performance of power generation and power distribution industries for the period 2008-09 to 2017-18. The study found disappointing liquidity performance with respect to the current ratio for both industries. However, the precise liquidity performance (represented by the acid test ratio) of both sectors was found to be acceptable during the period under study. The study further observed that on average, the liquidity performance of both industries was the same, as indicated by Fisher’s t-test.

Richard and Kalyani (2019) carried out an empirical study on the financial distress of selected PSEs in India based on fifteen fiscal ratios from a sample of fifteen companies. The study applied a cubic trend investigation process to measure the fiscal distress through the financial ratios selected in the study. The findings of the study revealed positive financial ratios among the distressed and non-distressed firms. It suggested that PSEs in India may become financially sound if they establish a good system of financial management. Further, the study helped by forecasting the overall financial health of the selected companies under study.

Singh (2020) explored the impact of disinvestment on the performance of CPSEs. The study noted that profit should not be the only criterion for the examination of public enterprises since CPSEs are also launched by the government for social welfare reasons. A change in the ownership or sale of a minority stake cannot be the single answer. The study concluded that the performance of the public enterprises improved significantly during the study period.

Ghosh (2020) attempted to analyze the expenditure and net profit trends of the CPSEs during the period 2010-11 to 2017-18. On the whole, the study concluded that there was a rising trend with respect to total expenditure and net profit after tax during the first four years under study. On average, the study observed that the growth rate in net profit after tax was higher than the growth rate in total expenditure. Thus, the CPSEs managed their total expenditure efficiently during the study period.

Bansal, Misra, and Tandon (2020) examined the working capital management of CPSEs during the post-financial crisis period, i.e., from 2010-11 to 2017-18. The study used secondary data. To analyze the relevant time series data, statistical and econometric techniques were used.The study concluded that Indian CPSEs managed their running funds proficiently (excluding the last year) in the post-financial crisis period, even though they adopted a hostile current resources strategy. Furthermore, the CPSEs had a positive impact on profitability. However, the turnover of working capital should be improved to generate liquidity effectively in the years ahead.

Ghosh (2020) evaluated the cash management performance of CPSEs in India from 2011-12 to 2017-18. To carry out the study, secondary data were collected at the aggregate level from the published annual reports of the Public Enterprises Survey for the selected study period. Linear regression and a Chi-square test were used to analyze the findings of the study. The results revealed that CPSEs in India sufficiently maintained and utilized their cash balances during the period under study.

Behera and Dhal (2020) analyzed the impact of ERP systems on the fiscal performance of CPSEs in the mineral and metal sectors. The study observed that some ratios performed better, which implied that there was a significant financial impact on the CPSEs that had adopted an ERP system. The study however suffered from the limitation of a shorter time period, since the effects of ERP implementation required more time to manifest.

Choudhary, Singh, and Gupta (2021) studied the impact of disinvestment on the fiscal performance of twenty CPSEs. The study observed a positive impact on the fiscal performance of CPSEs in India in terms of liquidity, dividend, value, and size. On the other hand, the profitability, leverage, and operational effectiveness of the CPSEs did not change significantly.

4. Objective of the Study

The primary aim of this study is to inspect whether industry-wise investment returns influence the aggregate investment returns of CPSEs in India.

5. Conceptual Model and Hypothesis of the Study

Based on the study’s objective, a conceptual model has been created to develop the study’s hypothesis. The conceptual model is presented in Figure 1.

Figure 1. Conceptual model for hypothesis development.

In accordance with the conceptual model shown above, the null and alternative hypotheses that have been developed for the study are presented below:

Null Hypothesis (H0): There is no significant influence of industry-wise investment returns on aggregate investment returns.

Alternative Hypothesis (HA): H0 is not true.

6. Research Design

6.1. Sample Design and Sample Selection

To determine the sample of the study, we must first define the population of our study. The population comprises all CPSEs in India. Based on the availability of data, the sample of the study comprises all the working CPSEs in India except the public enterprises that run on a departmental basis, indemnity companies, and banking companies. The year-wise number of operating CPSEs for the selected study period (mentioned in section 3.4) is shown in Table 1.

| Years | 2010-2011 |

2011-2012 |

2012-2013 |

2013-2014 |

2014-2015 |

2015-2016 |

2016-2017 |

2017-2018 |

2018-2019 |

2019- 2020 |

| No. of operating CPSEs | 220 |

225 |

229 |

234 |

235 |

244 |

257 |

257 |

249 |

256 |

Source: Published Annual Reports of Public Enterprises Survey from 2010-11 to 2019-20 of the Department of Public Enterprises, Government of India, New Delhi. Retrieved from https://dpe.gov.in/publication/pe-survey/pe-survey-report. |

Hence, the chosen sample size may be considered sufficient and representative.

To gain a general idea of the coverage of the chosen sample, it is imperative to categorize the selected study sample. For the present study, the selected sample is classified into 20 different industries, including 13 industries in the manufacturing sector and 7 industries in the service sector. The classification of the selected sample is shown in Table 2:

| Manufacturing Sector | |

1 |

Agro Industry (AI) |

2 |

Coal Industry (CI) |

3 |

Crude Oil Industry (COI) |

4 |

Other Minerals & Metals Industry (OMMI) |

5 |

Steel Industry (SI) |

6 |

Petroleum (Refinery & Marketing) Industry (PRMI) |

7 |

Fertilizers Industry (FI) |

8 |

Chemicals & Pharmaceuticals Industry (CPI) |

9 |

Heavy & Medium Engineering Industry (HMEI) |

10 |

Transportation Vehicle & Equipment Industry (TVEI) |

11 |

Industrial and Consumer Goods Industry (ICGI) |

12 |

Textiles Industry (TI) |

13 |

Power Generation Industry (PGI) |

| Service Sector | |

14 |

Power Transmission Industry (PTI) |

15 |

Trading & Marketing Industry (TMI) |

16 |

Transport & Logistic Services Industry (TLSI) |

17 |

Contract & Construction and Tech. Consultancy Services Industry (CCTCSI) |

18 |

Hotel and Tourist Services Industry (HTSI) |

19 |

Financial Services Industry (FSI) |

20 |

Telecommunication & Information Technology Industry (TITI) |

Source: Published Annual Reports of Public Enterprises Survey from 2010-11 to 2019-20 of the Department of Public Enterprises, Government of India, New Delhi. Retrieved from https://dpe.gov.in/publication/pe-survey/pe-survey-report. |

6.2. Study Period

The selected study period runs from the financial year 2010-2011 to the financial year 2019-2020 on a rolling basis. The 10-year study period is long enough to draw attention to the financial situation of the industries as it covers the diverse phases of the trade cycle.

6.3. Data Source

The study is mainly based on secondary data. To carry out the study, the required data has been collected from the published annual reports of the Public Enterprises Survey, Government of India, from 2010-11 to 2019-20.

6.4. Methodology

To achieve the objective of the study, three popular investment ratios are used. They are measured by ROA, ROCE, and ROE. The ratios are calculated in the following way:

ROA = Net Profit after Taxes ÷ Total Assets

ROCE = EBIT ÷ Capital Employed

ROE = Net Profit after Taxes ÷ Shareholders’ Equity

To study the influence of industry-wise investment returns on the aggregate investment returns of the CPSEs, the independent and dependent variables to be considered are indicated below:

Independent Variables: Industry-wise investment returns in terms of ROA, ROCE, and ROE.

Dependent variables: Aggregate investment returns in terms of ROA, ROCE, and ROE.

6.5. The Linear Regression Model

To examine the influence of industry-wise investment returns on the aggregate investment returns of the CPSEs, a linear regression equation (Ghosh & Saha, 1987) has been fitted to the pertinent yearly time-series data. The linear regression equations that are applied are shown below:

ROA = a + b Xi + Ut

ROCE = a + b Xi + Ut

ROE = a + b Xi + Ut

Where:

ROA, ROCE, and ROE = dependent variables representing aggregate investment returns of the CPSEs.

a = intercept; b = regression coefficient; Xi = independent variables representing investment returns of each selected industry of the CPSEs; and Ut = error term (i.e., residual) of the equation.

The coefficients of the regression equations are tested using the popular t-test (Das, 1990).

Table 3. Linear regression analysis for industry-wise influence of investment returns on the aggregate investment returns of CPSEs in India from 2010-11 to 2019-20. |

| Selected Industries | R2 |

Regression Co-efficient (b) |

|||||

ROA |

ROCE |

ROE |

ROA |

ROCE |

ROE |

||

| Manufacturing Sector: | |||||||

| AI | 0.04 |

0.02 |

0.10 |

-0.03 i (-0.55) |

-0.04 i (-0.42) |

-0.01 i (-0.97) |

|

| CI | 0.11 |

0.13 |

0.15 |

0.06 i (1.01) |

0.08 i (1.09) |

-0.07 i (-1.18) |

|

| COI | 0.36 |

0.90 |

0.63 |

0.12 i (2.12) |

0.26*** (8.62) |

0.30*** (3.71) |

|

| OMMI | 0.11 |

0.68 |

0.48 |

0.06 i (0.98) |

0.18*** (4.08) |

0.30** (2.71) |

|

| SI | 0.04 |

0.44 |

0.41 |

0.04 i (0.57) |

0.16** (2.52) |

0.18** (2.36) |

|

| PRMI | 0.05 |

0.001 |

0.05 |

0.07 i (0.66) |

0.01 i (0.10) |

0.07 i (0.67) |

|

| FI | 0.08 |

0.002 |

0.14 |

0.01 i (0.82) |

0.002 i (0.12) |

-0.01 i (-1.15) |

|

| CPI | 0.35 |

0.16 |

0.002 |

-0.03 i (-2.08) |

-0.04 i (-1.25) |

-0.01 i (-0.14) |

|

| HMEI | 0.20 |

0.23 |

0.35 |

0.17 i (1.43) |

0.17 i (1.53) |

0.15 i (2.09) |

|

| TVEI | 0.22 |

0.78 |

0.47 |

0.28 i (1.49) |

0.23*** (5.32) |

0.17** (2.67) |

|

| ICGI | 0.10 |

0.45 |

0.26 |

-0.02 i (-0.96) |

0.04** (2.54) |

-0.08 i (-1.66) |

|

| TI | 0.36 |

0.21 |

0.13 |

0.03 i (2.10) |

0.02 i (1.46) |

0.01 i (1.11) |

|

| PGI | 0.59 |

0.49 |

0.26 |

0.67*** (3.41) |

0.85** (2.76) |

1.28 i (1.68) |

|

| Service Sector: | |||||||

| PTI | 0.03 |

0.45 |

0.16 |

-0.24 i (-0.47) |

-1.16** (-2.57) |

-0.53 i (-1.25) |

|

| TMI | 0.21 |

0.10 |

0.05 |

0.27 i (1.46) |

0.03 i (0.96) |

0.04 i (0.68) |

|

| TLSI | 0.19 |

0.85 |

0.39 |

-0.08 i (-1.35) |

-0.22*** (-6.66) |

-0.03 i (-2.26) |

|

| CCTCSI | 0.06 |

0.23 |

0.46 |

-0.56 i (-0.73) |

-0.53 i (-1.54) |

0.48** (2.63) |

|

| HTSI | 0.59 |

0.75 |

0.70 |

-0.14*** (-3.39) |

-0.08*** (-4.84) |

-0.13*** (-4.28) |

|

| FSI | 0.56 |

0.31 |

0.29 |

1.25** (3.16) |

0.64 i (1.88) |

0.50 i (1.82) |

|

| TITI | 0.18 |

0.08 |

0.36 |

0.08 i (1.33) |

0.07 i (0.84) |

0.11 i (2.13) |

|

Notes:

|

7. Findings and Analysis

In this section, an attempt is made to examine the influence of industry-wise investment returns on the aggregate investment returns of CPSEs in India. In this respect, the investment returns of each selected industry are taken as independent variables. On the other hand, the dependent variable is represented by the aggregate investment returns of the CPSEs.

7.1. Empirical Analysis

In terms of ROCE and ROE, it can be observed in Table 3 that COI, OMMI SI, and TVEI, within the manufacturing sector, have a significant positive influence on the aggregate investment returns of the CPSEs. These positive influences are found to be significant either at the 1% level or at the 5% level. Further, ICGI with respect to ROCE and PGI with respect to ROA and ROCE within the manufacturing sector have a significant positive influence on the aggregate investment returns of the CPSEs. On the other hand, PTI and TLSI within the service sector have a significant negative influence on the aggregate investment returns of the CPSEs with respect to ROCE. However, CCTCSI and FSI within the service sector show a significant positive influence, with respect to ROE and ROA respectively, on the aggregate investment returns of the CPSEs, while HTSI within the service sector has a significant negative influence on the aggregate investment returns of the CPSEs with respect to all the investment ratios selected in the study.

For the rest of the industries within the two sectors, the results are found to be insignificant during the period under study.

7.2. Statistical Inference

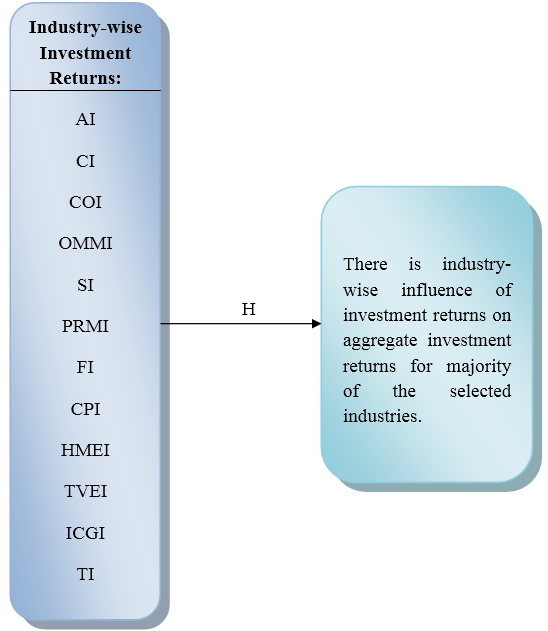

The above analysis leads to the acceptance of the null hypothesis of the study for AI, CI, PRMI, FI, CPI, HMEI, TI, TMI, and TITI, while rejecting the same null hypothesis for COI, OMMI, SI, TVEI, ICGI, PGI, PTI, TLSI, CCTCSI, HTSI, and FSI.

7.3. Outcome of the Conceptual Model

Based on the hypothesis that has been accepted in the study, the result of the conceptual model is presented in Figure 2:

Figure 2. Result of the conceptual model based on the accepted study hypothesis.

7.4. Results Divergent from Preceding Studies

The findings of prior studies have been to some extent contradictory; therefore, those studies were unable to establish with any certainty the impact of disinvestment on Indian CPSEs. Moreover, no prior studies were found on the industry-wise influence of investment income on the total investment income of CPSEs in the recent disinvestment environment. Also, no studies were found that concerned the aggregate level as well as the industry-wise level of the issue. Furthermore, the majority of the previous studies adopted a pre- and post-disinvestment approach to examining the impact of disinvestment on the fiscal performance of Indian CPSEs.

Hence, the results derived from the above analysis for the first time cast light on the effect of industry-wise investment income on the aggregate investment income of Indian CPSEs in the disinvestment environment.

8. Conclusion

On the whole, the results imply that few industries positively drive the performance of aggregate investment returns of CPSEs. Hence, the performance of aggregate CPSEs in terms of investment returns is mainly driven by the performance of COI, OMMI, SI, TVEI, ICGI, PGI, CCTCSI, and FSI. In terms of overall profitability (i.e., ROCE), PGI has the highest positive influence (0.85), while ICGI has the lowest positive influence (0.04) on the overall profitability of the aggregate CPSEs – values which are found to be significant at the 5% level.

From the results of the study, it is apparent that of the significant cases, most of the industries that positively influence the performance of aggregate investment returns of CPSEs fall within the manufacturing sector. Hence, the government may invest more funds in the industries within the manufacturing sector in order to achieve an optimal utilization of resources and generate a higher rate of return on their investment.

In India, CPSEs are considered the backbone of the nation’s fiscal growth. The present study has analyzed the influence of industry-wise investment returns on the aggregate investment returns of Indian CPSEs. Therefore, considering the importance of CPSEs in the Indian economy, the current study could be extended to the company level by selecting companies within each of the CPSEs’ industries.

References

Achini, A., & Begum, S. (2018). Impact of disinvestment on financial performance: A comparative study of Maharatna and Navratna companies. International Journal of Pure and Applied Mathematics, 118(15), 65-69.

Antony, M. T. (1992). Efficiency in central public sector enterprises in Kerala: An analysis of capacity utilization, profitability and productivity. Ph.D. Thesis. Department of Applied Economics, Cochin University of Science and Technology.

Bansal, R., Misra, S. K., & Tandon, D. (2020). Working capital management of central public sector enterprises (CPSEs) in India during the post-financial recession period: Empirical evidence on aggregation. Journal of Critical Reviews, 7(15), 1455-1462.

Batth, C. V., Nayak, B., & Pasumarti, S. S. (2018). The study of financial performance of Indian public sector undertakings. Global Journal of Finance and Management, 10(1), 21-43.

Behera, R. K., & Dhal, S. K. (2020). The impact of ERP systems on financial performance of central public sector enterprises working in mineral and metal sector. International Journal of Recent Technology and Engineering, 9(2), 144-149.

Cadoret, J. (2016). Empirical study on the effect of the return on investment on budgetary slacks in investment expenditures. Master’s Thesis. Dijon School of Management, University of Burgundy.

Choudhary, V. K., Singh, K., & Gupta, V. (2021). Impact of disinvestment on performance of select central public sector enterprises in India. Mudra: Journal of Finance and Accounting, 8(2), 1-19.Available at: https://doi.org/10.17492/jpi.mudra.v8i2.822101.

Das, N. G. (1990). Statistical methods (Vol. 2). Kolkata: M.Das & Co.

Galal, A. (1994). Welfare consequences of selling public enterprises: An empirical analysis. Washington DC: Oxford University Press for the World Bank.

George, E., & Vinod, R. (2016). A study on the performance of central public sector enterprises in India. International Journal of Engineering Science and Computing, 6(5), 5267-5271.

Ghosh, R., & Saha, S. (1987). Business mathematics & statistics (5th ed. Vol. 1). Kolkata: New Central Book Agency.

Ghosh, S. (2019a). Liquidity performance of central power sector enterprises in India: A comparative study between power generation and power transmission industries. PIMT Journal of Research, 12(1), 1-6.

Ghosh, S. (2019b). Performance appraisal through inventory management: The case of central public sector enterprises (CPSEs) in India. The Management Accountant, 54(7), 103-109.Available at: https://doi.org/10.33516/maj.v54i7.103-109p.

Ghosh, S. (2020). Cash management of central public sector enterprises in India: A macro level study. PIMT Journal of Research, 12(3), 30-34.

Ghosh, S. (2020). Expenditure and net profit trends of central public sector enterprises (CPSEs) in India: An empirical analysis. Studies in Indian Place Names, 40(60), 6474-6479.

Khan, M. Y., & Jain, P. K. (1994). Financial management – text and problems (2nd ed.). New Delhi: Tata McGraw-Hill Publishing Company Limited.

Kumar, R. S. (2017). Disinvestment of public sector units in India: A strategic analysis. Paper presented at the 6th International Conference on Emerging Trends in Engineering, Technology, Science and Management. Institution of Electronics and Telecommunication Engineers, Bengaluru, Karnataka, India.

Mandiratta, P., & Bhalla, G. (2017). Pre and post disinvestment performance evaluation of Indian CPSEs. Management and Labour Studies, 42(2), 120-134.Available at: https://doi.org/10.1177/0258042x17716601.

Megginson, W. L., & Netter, J. M. (2001). From state to market: A survey of empirical studies on privatization. Journal of Economic Literature, 39(2), 321-389.Available at: https://doi.org/10.1257/jel.39.2.321.

Patnaik, I. (2007). PSU disinvestment. Retrieved from http://www.India-seminar.com/2006/557/557%20ila%20patnaik.htm .

Rastogi, M., & Shukla, S. (2013). Challenges and impact of disinvestment on Indian economy. International Journal of Management & Business Studies, 3(4), 44-53.

Ray, K., & Maharana, S. (2002). Restructuring PSEs through disinvestment: Some critical issues, Pratibimba. Journal of Management Information Systems, 2(2), 56-62.

Richard, P. V., & Kalyani, B. (2019). Empirical analysis of financial distress of selected public sector undertakings in India. International Journal of Business and Management Invention, 8(4), 30-38.

Sankar, T. L., & Reddy, Y. V. (1989). Privatization: Diversification of ownership of public enterprises. Hyderabad: Institute of Public Enterprise. Booklinks Corporation.

Sharma, P. (2016). Impact of disinvestment on financial performance of PSEs in India. International Journal of Science, Technology and Management, 5(8), 610-616.

Singh, A. (2017). Financial performance of central public sector enterprises in India. International Research Journal of Management and Commerce, 4(3), 1-37.

Singh, G. (2015). Disinvestment and performance of profit and loss making Central public sector enterprises of India. Indian Journal of Research, 4(4), 2250-1991.

Singh, G., & Paliwal, D. (2010). Impact of disinvestment on the financial and operating performance of competitive and monopoly units of Indian public sector enterprises. International Journal of Research in Commerce and Management, 1(2), 40-57.

Singh, R. A. (2020). Disinvestment and its impact on the performance of CPSEs. International Journal of Trend in Scientific Research and Development, 4(6), 1293-1299.